Europe Digital Payment Market Size, Share and Trends, 2034

Europe Digital Payment Market Report Summary

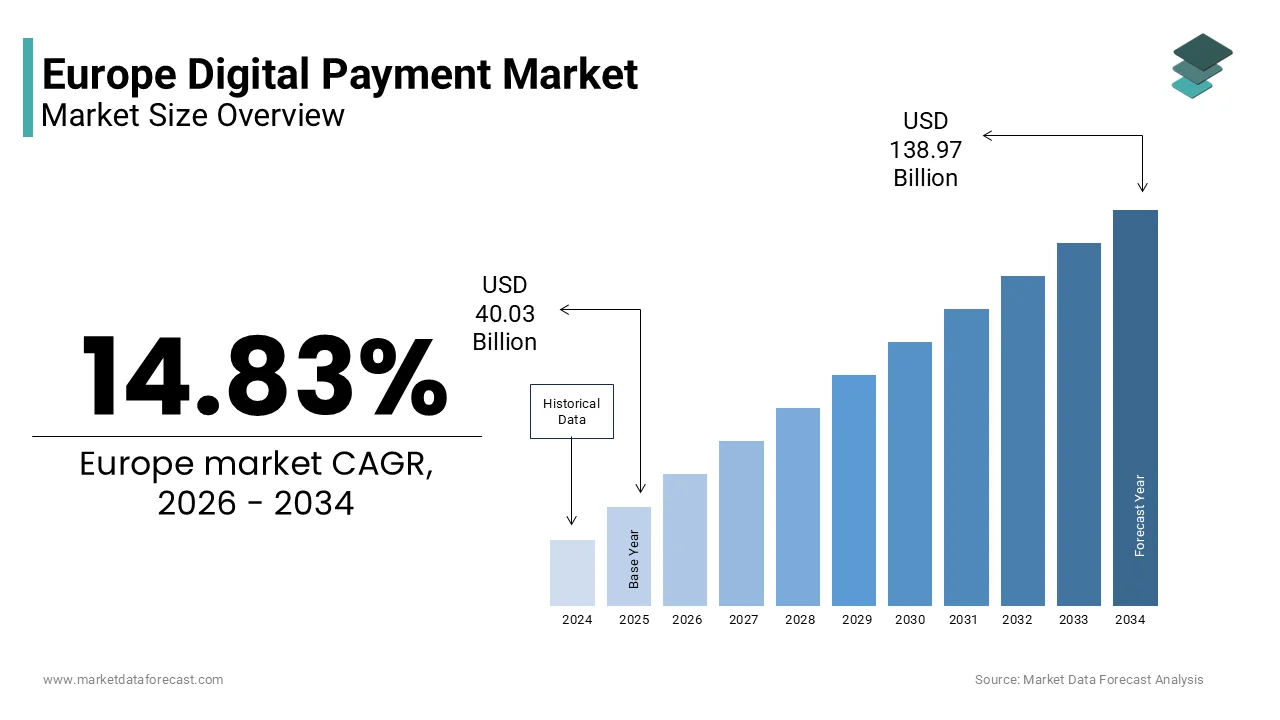

The Europe digital payment market was valued at USD 40.03 billion in 2025, is estimated to reach USD 45.97 billion in 2026, and is projected to reach USD 138.97 billion by 2034, growing at a CAGR of 14.83% during the forecast period. The growth of the Europe digital payment market is driven by the increasing adoption of cashless transactions, rapid expansion of e commerce platforms, and rising use of mobile wallets and contactless payment technologies. Digital payment systems enable consumers and businesses to conduct secure and convenient financial transactions through online platforms, mobile devices, and payment gateways. The increasing penetration of smartphones, improvements in financial technology infrastructure, and strong regulatory support for digital financial services are further accelerating the adoption of digital payments across Europe.

Key Market Trends

- Increasing consumer preference for contactless and mobile based payment methods for everyday transactions.

- Rapid expansion of e commerce platforms and digital marketplaces supporting online payment solutions.

- Growing adoption of mobile wallets and real time payment technologies across European countries.

- Rising integration of advanced security technologies such as biometric authentication and tokenization to improve transaction safety.

- Expansion of fintech innovation and digital banking platforms offering seamless payment services.

Segmental Insights

- Based on component, the software segment dominated the Europe digital payment market and accounted for 66.5% of the regional market share in 2025. Payment software platforms play a crucial role in processing digital transactions, managing payment gateways, and enabling secure online financial operations.

- Based on organization size, the large enterprises segment held the largest share of the Europe digital payment market and captured 60.6% of the regional market share in 2025. Large organizations widely adopt digital payment systems to manage high transaction volumes, streamline financial operations, and support global digital commerce activities.

- Based on vertical, the banking, financial services, and insurance segment retained the largest share of the Europe digital payment market and accounted for 36.5% of the regional market share in 2025. Financial institutions are major adopters of digital payment technologies to enhance transaction efficiency, improve customer experience, and expand digital banking services.

Regional Insights

- The Europe digital payment market is witnessing strong growth across several countries due to the increasing adoption of digital financial services and cashless payment technologies.

- The United Kingdom accounted for the largest share of the Europe digital payment market and held 24.4% of the regional market share in 2025. The country’s strong fintech ecosystem, widespread use of contactless payments, and advanced digital banking infrastructure are key factors supporting market growth.

- Other European countries are also experiencing rapid growth in digital payment adoption supported by expanding e commerce activities, increasing smartphone usage, and the growing popularity of mobile payment platforms.

Competitive Landscape

The Europe digital payment market is highly competitive with the presence of global fintech companies, payment service providers, and financial institutions. Companies are focusing on developing secure payment platforms, expanding cross border payment capabilities, and integrating advanced technologies such as artificial intelligence and blockchain to improve transaction efficiency. Strategic partnerships with banks, merchants, and digital platforms are helping companies strengthen their presence in the European digital payment ecosystem. Prominent players in the Europe digital payment market include PayPal, Square, Adyen, Stripe, Alipay, WeChat Pay, Visa, Mastercard, American Express, and Revolut.

Europe Digital Payment Market Size

The Europe digital payment market size was valued at USD 40.03 billion in 2025 and is projected to reach USD 138.97 billion by 2034 from USD 45.97 billion in 2026, growing at a CAGR of 14.83%.

Digital payment encompasses electronic transaction mechanisms that facilitate monetary exchanges through digital channels including mobile applications, online platforms, and contactless infrastructure across European Union member states and associated economies. This ecosystem integrates card networks, digital wallets, real time bank transfers, and emerging central bank digital currency frameworks to enable secure, efficient, and instantaneous value transfer between consumers, merchants, and financial institutions. According to the European Central Bank, the total number of non-cash payment transactions in the euro area reached a very high level in the first half of 2025, reflecting steady growth compared to the prior year period. As per the European Court of Auditors, the value of digital payments for retail sales in the European Union exceeded significant thresholds annually by 2023, demonstrating strong economic integration of digital transaction methods. The shift toward cashless behavior is further evidenced by European Central Bank data indicating that cash usage at physical points of sale has declined considerably over the past decade. Digital payment adoption varies across regions, with the Netherlands recording a majority of point-of-sale transactions conducted via card or mobile applications, while countries such as Malta and Austria maintain cash usage levels above half of all transactions according to payment attitude surveys published by the European Central Bank. This heterogeneous landscape underscores the interplay of technological infrastructure, regulatory frameworks, and consumer preferences shaping Europe’s digital payment evolution.

MARKET DRIVERS

Expanding Smartphone Penetration and Digital Literacy Accelerating Mobile Payment Adoption

The proliferation of smartphones and enhanced digital competencies across European populations is majorly driving the growth of the European digital payment market. According to Eurostat, internet usage among individuals in the European Union reached very high levels in 2024, with mobile devices accounting for the majority of online access points. As per the European Central Bank, mobile payment transactions at physical points of sale have grown significantly since 2016, which is reflecting strong adoption momentum. Younger demographics demonstrate particularly strong engagement, with individuals aged 18 to 34 showing high mobile payment usage rates in Western European markets as per YouGov and Brite Payments research. Furthermore, digital literacy initiatives supported by the European Commission’s Digital Education Action Plan have equipped citizens with the skills necessary to navigate secure digital transaction environments. As per Capgemini Research Institute, countries achieving high smartphone penetration demonstrate digital payment transaction volumes several times higher than markets with lower device adoption.

Regulatory Frameworks Promoting Open Banking and Payment Innovation

The implementation of the Revised Payment Services Directive and associated open banking regulations has fundamentally transformed Europe’s payment landscape, which is also propelling the expansion of the European digital payment market. According to the European Banking Authority, hundreds of licensed payment initiation service providers operated within the European Economic Area by 2025, which is enabling consumers to initiate payments directly from bank accounts without traditional card intermediaries. As per YouGov and Brite Payments, Pay by Bank solutions were preferred by a significant portion of Western European consumers for online transactions in 2024. According to the European Central Bank, instant credit transfers processed through retail payment systems accounted for a notable share of total credit transfer volumes in the first half of 2025, which is reflecting rapid adoption of real time settlement capabilities. Furthermore, the EU Instant Payments Regulation adopted in March 2024 mandates that payment service providers enable instant transfer capabilities by October 2025. As per the European Court of Auditors, these regulatory interventions have contributed to reducing transaction costs and enhancing competition among providers, while strengthening consumer protection through standardized authentication protocols.

MARKET RESTRAINTS

Data Privacy Concerns and GDPR Compliance Complexities Limiting Consumer Confidence

Stringent data protection requirements under the General Data Protection Regulation create operational challenges for digital payment providers while influencing consumer willingness to adopt electronic transaction methods, which is significantly impeding the growth of the European digital payment market. According to the European Data Protection Board, payment service providers must implement rigorous data minimization, purpose limitation, and consent management protocols that increase compliance costs and technical complexity. According to the research published by the International Monetary Fund, GDPR compliance expenditures for financial technology firms in Europe represent a significant portion of annual operational budgets. Consumer apprehension regarding personal financial data usage remains strong, with the European Central Bank reporting that many respondents cite privacy protection as the primary advantage of cash transactions. Furthermore, cross border data transfer restrictions under GDPR complicate the development of pan European payment solutions, as providers must navigate varying national interpretations of data protection requirements. As per the European Court of Auditors, these regulatory complexities can delay deployment of innovative payment services and increase barriers to entry for smaller providers.

Fragmented National Payment Preferences and Legacy Infrastructure Impeding Harmonization

Europe’s diverse payment culture and heterogeneous technological infrastructure present obstacles to unified digital payment adoption, which is hampering the regional market expansion. According to GR4VY analysis, local payment schemes such as iDEAL in the Netherlands, BLIK in Poland, and Bizum in Spain collectively process billions of transactions annually, which is creating entrenched consumer preferences that resist migration to pan European solutions. According to the European Central Bank, card payment acceptance rates at physical points of sale vary widely across member states, reflecting uneven infrastructure development. Legacy banking systems in several countries require modernization to support real time payment capabilities, with the European Commission estimating that infrastructure upgrades across the euro area could be very costly. As per yStats research, Eastern European markets demonstrate lower digital wallet adoption rates compared to Western counterparts, despite growing smartphone penetration. This fragmentation increases operational complexity for merchants seeking consistent payment experiences across Europe, often necessitating integration with multiple local schemes alongside international card networks. Varying national regulations regarding authentication, transaction limits, and consumer protection further slow cross border innovation. The coexistence of advanced digital ecosystems and cash dependent economies requires nuanced strategies that respect local preferences while advancing broader digitalization objectives.

MARKET OPPORTUNITIES

Central Bank Digital Currency Development and Digital Euro Initiative Creating New Transaction Paradigms

The European Central Bank’s advancement of a digital euro offers a promising opportunity for the European digital payment market. According to European Central Bank publications, the digital euro project aims to provide citizens with a public digital payment option that complements private sector solutions while ensuring monetary sovereignty and financial stability. The Consumer Expectations Survey conducted by the ECB shows that awareness of the digital euro has grown significantly in recent years, reflecting increasing public engagement. As per the International Monetary Fund, a well-designed central bank digital currency could enhance payment system resilience, reduce dependency on non-European providers, and facilitate more efficient cross border transactions. The European Commission’s retail payments strategy emphasizes the importance of public digital payment options in fostering competition and innovation. This initiative also presents opportunities for European technology providers to lead in secure transaction infrastructure, potentially generating economic value and export capabilities.

Cross Border Payment Harmonization Through SEPA Instant Payments Expansion

The expansion of the Single Euro Payments Area (SEPA) instant credit transfer framework presents substantial opportunities in the European digital payment market. According to the European Central Bank, TARGET Instant Payment Settlement processed a rapidly increasing number of transactions in 2024, demonstrating the scaling of instant payment infrastructure. The EU Instant Payments Regulation mandates that all payment service providers enable instant transfer capabilities by October 2025, which is creating a unified foundation for immediate fund availability. As per GR4VY analysis, real time payment adoption is accelerating in Eastern European markets, with systems such as Poland’s BLIK and Spain’s Bizum gaining widespread usage. As per the European Court of Auditors, enhanced instant payment capabilities could significantly reduce transaction costs compared to traditional cross border methods, generating efficiency gains for businesses and consumers. Furthermore, instant payment infrastructure supports emerging use cases including request to pay functionality, integrated invoicing, and automated treasury management. As adoption deepens, convergence with open banking frameworks could enable innovative financial services leveraging real time transaction data for personalized offerings and financial planning tools.

MARKET CHALLENGES

Escalating Cybersecurity Threats and Fraud Prevention Demands in Digital Transaction Environments

The rapid expansion of digital payment channels has intensified cybersecurity risks and fraud prevention challenges that threaten consumer trust and market stability, which is a significant challenge to the growth of the European digital payment market. According to UK Finance and Accenture research, authorized push payment fraud losses in the United Kingdom reached significant levels in 2023, highlighting the sophistication of social engineering and account takeover attacks. The European Central Bank reports that while card fraud rates in the Single Euro Payments Area have declined, the absolute volume of fraudulent transactions continues to grow alongside adoption. As per the European Union Agency for Cybersecurity, payment service providers face increasing pressure to implement multi factor authentication, behavioral analytics, and real time fraud detection systems. The European Court of Auditors emphasizes that robust cybersecurity frameworks are essential for maintaining consumer confidence in digital payment systems. Addressing these challenges requires collaboration between financial institutions, technology providers, law enforcement agencies, and regulators to develop adaptive security protocols that evolve alongside emerging threats.

Digital Divide Affecting Inclusive Payment Access Across Demographics and Regions

Persistent disparities in digital access, skills, and infrastructure create challenges for the European digital payment market. According to the European Central Bank’s payment attitudes survey, a notable share of euro area consumers report requiring assistance with digital payment methods, with older adults and individuals with lower education or income levels demonstrating higher dependency rates. The European Commission’s Digital Economy and Society Index indicates that while a majority of EU internet users purchased goods or services online in 2024, gaps remain in digital literacy and connectivity between urban and rural areas. As per Eurostat, individuals with lower educational attainment are significantly more likely to lack basic digital skills necessary for secure online transactions. Furthermore, cash dependency remains pronounced in certain regions, with the ECB noting that cash usage exceeds 60% of point-of-sale transactions in countries such as Malta, Austria, and Slovenia. Addressing these challenges requires coordinated efforts to enhance digital skills training, improve broadband accessibility, and ensure payment solutions accommodate diverse user needs including offline functionality and simplified interfaces. The EU’s Digital Education Action Plan and cohesion policy investments represent important steps toward bridging these gaps, but sustained commitment will be essential to ensure equitable access.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

14.83% |

|

Segments Covered |

By Component, Deployment Model, Vertical, Vertical, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

PayPal (US), Square (US), Adyen (NL), Stripe (US), Alipay (CN), WeChat Pay (CN), Visa (US), Mastercard (US), American Express (US), Revolut (GB) |

SEGMENTAL ANALYSIS

By Component Insights

The software segment led the market by commanding for 66.5% of the European market share in 2025. The dominance of software segment in the European market is attributed to the critical reliance on secure transaction processing platforms, fraud detection algorithms, and cloud-based payment gateways that form the backbone of modern digital finance. Unlike hardware which requires physical deployment, software solutions offer scalability and rapid updates essential for adapting to evolving regulatory standards and consumer preferences. The imperative to adhere to stringent European security standards such as Strong Customer Authentication under the Revised Payment Services Directive has propelled massive investment in payment software infrastructure. According to the European Banking Authority, most payment service providers upgraded their authentication software frameworks between 2023 and 2025 to meet compliance deadlines. As per Capgemini Research Institute, expenditure on cybersecurity software within the European financial sector continued to grow during this period, reflecting the urgent need to combat sophisticated fraud schemes. The software segment benefits from the shift toward tokenization and encryption technologies that protect sensitive cardholder data during transmission. According to the International Monetary Fund, banks in the euro area allocated a significant portion of their technology budgets specifically to regulatory technology software in 2024. This sustained focus on compliance ensures that software remains the primary cost center and value driver, as institutions prioritize agile, updatable systems over static hardware to maintain operational resilience against emerging cyber threats across the single market.

The hardware segment is projected to register a promising CAGR of 12.2% over the forecast period in this regional market. Factors such as the massive rollout of contactless Point of Sale terminals and the integration of biometric verification devices across retail and hospitality sectors are propelling the expansion of hardware segment in the European market. The widespread mandate for contactless acceptance and the expiration of legacy magnetic stripe technologies have triggered a comprehensive refresh cycle for Point-of-Sale hardware across Europe. According to the European Central Bank, the number of contactless enabled terminals in the euro area surpassed millions of units in 2024, which is showing strong growth as merchants adapted to consumer demand for tap and go transactions. As per RBR Limited, the replacement rate for payment terminals in Western Europe reached a decade high, with large volumes of new devices shipped in 2024 to support higher transaction limits and enhanced security chips. The shift toward soft POS solutions running on commercial off the shelf smartphones also contributes to hardware volume, blurring the lines but still requiring certified secure elements. According to the European Court of Auditors, public sector initiatives to digitize small merchant payments subsidized terminal acquisitions in Southern and Eastern European markets, further boosting shipment volumes. This hardware renewal is not merely a replacement exercise but an upgrade to devices capable of handling complex protocols like EMV 3DS and QR code scanning. The sheer volume of physical touchpoints required to serve the millions of micro merchants entering the digital ecosystem ensures that hardware procurement will outpace other segments in terms of unit growth rates over the forecast period.

By Organization Size Insights

The large enterprises segment led the market by capturing 60.6% of the regional market share in 2025. The dominance of large enterprises segment in the European market can be credited to their extensive merchant networks, high transaction volumes, and the capacity to invest in sophisticated, customized payment orchestration platforms that manage complex global supply chains and omnichannel strategies. Large corporations operate intricate sales ecosystems spanning physical stores, e-commerce portals, mobile apps, and marketplaces, which is requiring advanced payment orchestration layers that only enterprise grade solutions can provide. According to McKinsey and Company, most of Europe’s largest retailers utilize multi acquirer strategies to optimize authorization rates and reduce processing costs, which is a complexity that demands robust software infrastructure. As per Forrester Research, large enterprises in the region allocate substantial budgets annually to payment technology maintenance and innovation, far exceeding the budgets of smaller counterparts. The European Retail Round Table indicates that top tier retailers process billions of transactions annually, requiring systems capable of handling peak loads during seasonal events like Black Friday without latency. These organizations also drive the adoption of value-added services such as dynamic currency conversion and integrated loyalty programs which are bundled into enterprise payment contracts. The need for seamless reconciliation across multiple jurisdictions and currencies further cements the reliance on specialized enterprise platforms. Consequently, the sheer scale of operations and the strategic importance of payment data analytics ensure that large enterprises remain the primary revenue source for payment service providers and technology vendors across the continent.

The small and medium enterprise segment is anticipated to witness the fastest CAGR of 14.4% over the forecast period owing to the rapid democratization of payment technologies, government digitization incentives, and the shifting consumer expectation for digital payment options even at micro merchant locations. The advent of payment aggregators and software-based Point of Sale solutions has drastically lowered the barrier to entry for small businesses, enabling them to accept digital payments with minimal upfront investment. According to the European Small Business Alliance, millions of small merchants in Europe adopted digital payment acceptance tools in 2024, showing strong growth largely driven by plug and play solutions from providers like SumUp and Square. As per Worldpay from FIS, the adoption of Soft POS technology, which turns smartphones into payment terminals, grew significantly among micro merchants in Southern Europe where traditional terminal penetration was historically low. These solutions eliminate the need for long term contracts and complex integration, allowing street vendors and service providers to transact digitally instantly. According to the European Commission, the Digital Single Market strategy has further supported this trend by promoting interoperable and low-cost payment options for SMEs. The ease of onboarding and transparent pricing models have empowered small businesses to participate in the cashless economy, driving a surge in transaction volumes from this previously underserved segment. This technological leveling field ensures that SMEs will contribute disproportionately to future market growth as digital habits permeate every corner of the retail landscape.

By Vertical Insights

The BFSI segment retained as the largest segment in the Europe digital payment market by holding 36.5% of the regional market share in 2025. The leading position of BFSI segment in the European market is driven by the sector’s role as the primary issuer of payment instruments, the operator of clearing infrastructure, and the guardian of regulatory compliance, which is making it the central hub of the digital payment value chain. Banks and financial institutions are undertaking massive digital transformation programs to replace legacy core banking systems with agile, cloud native platforms capable of supporting real time payments and open banking APIs. According to Deloitte, European banks plan to invest heavily in technology modernization by 2026, with a significant portion dedicated to payment processing engines and digital wallet integration. As per the European Banking Federation, most major banks in the region have launched or upgraded their mobile banking applications in the last two years to include advanced payment features such as peer to peer transfers and bill payments. According to the International Monetary Fund, the shift toward open banking has compelled banks to expose their payment infrastructure securely, creating new revenue streams through API monetization. The necessity to maintain sovereignty over customer data and transaction flows keeps investment levels in this vertical consistently higher than in any other industry segment.

The retail and e-commerce segment is projected to witness a prominent CAGR of 15.1% over the forecast period. The irreversible shift toward omnichannel shopping behaviours, the proliferation of buy now pay later services, and the integration of embedded finance into online customer journeys are propelling the retail and e-commerce segment in the European market. The blurring of lines between physical and digital retail has created an insatiable demand for unified payment solutions that offer a seamless experience regardless of the channel. According to Euromonitor International, online retail sales in Europe accounted for a significant share of total retail turnover in 2024, driving a corresponding surge in digital payment gateway usage and mobile wallet adoption. As per Stripe research, a majority of European consumers expect to use the same payment method online and in store, pushing retailers to adopt integrated Point of Sale and e-commerce platforms. According to the European E-commerce Association, cross border online shopping within the EU grew strongly in 2024, necessitating multi-currency and local payment method support. Retailers are investing heavily in payment orchestration to optimize conversion rates and reduce cart abandonment. This relentless expansion of digital touchpoints and the consumer demand for frictionless checkout experiences ensure that the retail vertical will outpace all others in growth rate as it continues to digitize every aspect of the shopping journey.

REGIONAL ANALYSIS

United Kingdom Digital Payment Market Analysis

The United Kingdom stood as the preeminent leader in the European digital payment market with 24.4% of the regional market share in 2025. The UK is serving as a global hub for fintech innovation and adoption. The nation’s status is defined by its advanced infrastructure, high consumer readiness, and a regulatory environment that has historically fostered rapid experimentation with new payment technologies. According to UK Finance, contactless payments accounted for a significant share of face-to-face card transactions in 2024, reflecting a deeply ingrained cashless culture among British consumers. As per the Financial Conduct Authority, the UK hosts thousands of active fintech firms, many of which specialize in digital payment solutions, creating a vibrant ecosystem that drives continuous market evolution. The Bank of England’s proactive stance on Central Bank Digital Currency research and real time gross settlement systems has further solidified the country’s technical leadership. According to NielsenIQ, mobile wallet transaction volumes have grown strongly since 2022. Furthermore, the widespread adoption of Faster Payments infrastructure enables instant fund transfers 24 hours a day, setting a benchmark for efficiency. Despite post Brexit regulatory divergences, the UK maintains its dominance through strong venture capital inflows and a consumer base that eagerly embraces digital financial tools, ensuring its position as the primary engine of growth for the wider European region.

Germany Digital Payment Market Analysis

Germany held a promising share of the European digital payment market in 2025. Factors such as a unique trajectory where traditional caution is rapidly giving way to digital acceleration driven by regulatory shifts and infrastructure modernization is primarily driving the German market expansion. Historically known for its cash preference, the German market is undergoing a profound transformation as the Electronic Cash system evolves and real time payment adoption surges. According to the Deutsche Bundesbank, cashless transactions in Germany grew significantly in 2024 as consumers shifted habits following the pandemic. As per Bitkom, the German digital association, most online shoppers now prefer digital payment methods over cash on delivery, signaling a decisive change in e-commerce behavior. The implementation of the EU Instant Payments Regulation is acting as a catalyst, with German banks aggressively upgrading their systems to support immediate transfers by the 2025 deadline. The popularity of local schemes like Girocard is being complemented by the rapid uptake of mobile wallets and Buy Now Pay Later services. According to the Federal Ministry of Finance, government initiatives to digitize public services and reduce administrative burdens are also pushing businesses toward digital settlement. This convergence of regulatory pressure, changing consumer sentiment, and robust industrial demand for efficient B2B payment solutions is propelling Germany’s market share upward, closing the gap with more advanced neighbors.

France Digital Payment Market Analysis

France is estimated to account for a prominent share of the European digital payment market during the forecast period. The French market is distinguished by a strong state led push toward digital sovereignty and the widespread success of domestic payment schemes that rival international giants. The French market is notable for its high penetration of contactless cards and the rapid integration of mobile payment solutions into daily commerce. According to the Banque de France, contactless payments represented a significant share of card transactions at physical points of sale in 2024, driven by the ubiquity of the CB network. As per Fevad, the federation of e-commerce and distance selling, digital payment usage in French online retail grew strongly in 2024, fueled by the adoption of secure 3D Secure 2.0 protocols that enhance consumer trust. The French government’s commitment to reducing cash usage through legislative caps on cash transactions for residents has further accelerated the shift toward electronic methods. The emergence of Lyf Pay and other homegrown mobile wallet solutions demonstrates a strategic effort to maintain control over payment data and infrastructure. According to the Autorité de Contrôle Prudentiel et de Résolution, French banks are investing heavily in open banking APIs to foster innovation while maintaining security. This blend of robust domestic infrastructure, supportive regulation, and a tech savvy population ensures France remains a critical pillar of the European digital payment ecosystem.

Italy Digital Payment Market Analysis

Italy is expected to exhibit a healthy CAGR in the European digital payment market during the forecast period. Italy is exhibiting a dynamic growth pattern driven by aggressive government incentives to combat tax evasion and modernize its historically cash heavy economy. The Italian market is experiencing a renaissance in digital payments as legislative measures and consumer benefits converge to alter long standing behaviors. According to the Bank of Italy, electronic payments increased significantly in 2024 as a direct result of the “Cashback Italia” program and strict limits on cash transactions for individuals and businesses. As per the National Institute of Statistics, the penetration of Point-of-Sale terminals among small merchants rose strongly in the last year, facilitated by simplified fiscal regimes for digital acceptance. The popularity of mobile payment apps like Satispay illustrates the success of localized solutions tailored to Italian consumer preferences. According to the Ministry of Economy and Finance, digital invoicing mandates have forced millions of small enterprises to adopt digital financial tracks, indirectly boosting payment digitization. Furthermore, the tourism sector’s recovery has spurred the adoption of contactless and multi-currency payment options in major cities. This top-down regulatory approach combined with bottom-up adoption of user-friendly apps is transforming Italy from a laggard into one of the fastest growing markets in Southern Europe.

Netherlands Digital Payment Market Analysis

The Netherlands is anticipated to account for a notable share of the European digital payment market during the forecast period. The Dutch market is characterized by the near total obsolescence of cash for daily transactions and the dominance of the iDEAL scheme which has become the gold standard for online banking payments. According to De Nederlandsche Bank, cash usage at points of sale dropped significantly in 2024, with debit card and mobile payments accounting for the overwhelming majority of transactions. As per Thuiswinkel.org, iDEAL processed hundreds of millions of transactions in 2024, capturing a dominant share of the e-commerce payment market and effectively marginalizing international card schemes for domestic online trade. The widespread adoption of Tikkie for peer-to-peer payments and bill splitting has further entrenched digital habits across all age groups. According to the Dutch Central Bank, the infrastructure for instant payments is fully operational and universally adopted, enabling real time settlement for virtually all transactions. The high level of digital literacy and trust in financial institutions creates an environment where new payment innovations are adopted almost instantly. This unparalleled maturity ensures that while the Netherlands may have a smaller absolute market size than larger economies, its density of digital payment activity and technological sophistication remain unmatched in the region.

COMPETITIVE LANDSCAPE

The competition in the Europe digital payment market is intensely dynamic characterized by a complex interplay between established banking giants agile fintech disruptors and global technology corporations. Traditional financial institutions leverage their extensive customer bases and regulatory expertise to maintain dominance while simultaneously modernizing legacy systems to compete with newer entrants. Fintech companies differentiate themselves through superior user experiences lower transaction fees and specialized niche solutions that address specific merchant needs effectively. Global tech firms utilize their vast ecosystems and data analytics capabilities to embed payment services directly into consumer applications creating seamless frictionless transactions. Regulatory frameworks like open banking have lowered entry barriers fostering an environment where innovation thrives and collaboration becomes essential for survival. Companies constantly vie for merchant loyalty by offering value added services such as advanced analytics loyalty programs and integrated lending solutions. The landscape sees frequent consolidation as larger players acquire innovative startups to accelerate technological adoption and expand their geographic reach across diverse European markets with varying consumer preferences

KEY MARKET PLAYERS

Some of the notable key players in the Europe digital payment market are

- PayPal (US)

- Square (US)

- Adyen (NL)

- Stripe (US)

- Alipay (CN)

- WeChat Pay (CN)

- Visa (US)

- Mastercard (US)

- American Express (US)

- Revolut (GB)

Top Players in the Market

- Adyen operates as a leading global payment platform headquartered in the Netherlands and serves as a critical infrastructure provider for major European enterprises. The company facilitates seamless omnichannel transactions by unifying online and physical point of sale systems into a single interface. Adyen recently strengthened its market position by expanding its issuing capabilities and launching enhanced data analytics tools that help merchants optimize authorization rates across the continent. The firm actively collaborates with major technology partners to integrate embedded finance solutions directly into enterprise resource planning systems. Its global contribution remains significant as it processes payments for iconic international brands while maintaining strict adherence to European regulatory standards. Adyen continues to invest heavily in fraud detection algorithms and real time risk management features to secure transactions for its diverse client base ranging from startups to multinational corporations.

- Nexi stands as a premier European payment technology group formed through strategic mergers and serves millions of users across Italy and broader European markets. The company provides a comprehensive suite of services including card processing digital banking solutions and merchant acquiring services. Nexi recently launched innovative open banking platforms that allow third party providers to access financial data securely under revised European directives. It has aggressively expanded its footprint by partnering with fintech startups to offer next generation mobile wallet solutions and contactless payment technologies. The group plays a vital role globally by setting benchmarks for secure transaction processing and interoperability within the Single Euro Payments Area. Nexi continuously upgrades its infrastructure to support instant payments and cross border settlements ensuring resilience against cyber threats while enhancing user experience for both consumers and merchants throughout the region.

- Worldline functions as a global leader in payment and transaction services with deep roots in France and extensive operations across Europe. The company delivers end to end solutions covering merchant services terminal networks and financial institution processing needs. Worldline recently accelerated its digital transformation by integrating artificial intelligence into its fraud prevention systems and launching cloud-based payment gateways for small businesses. It has forged strategic alliances with major card schemes to enable faster settlement times and improved currency conversion rates for cross border trade. The firm contributes significantly to the global market by pioneering sustainable payment technologies and reducing the carbon footprint of digital transactions. Worldline remains committed to innovation through continuous investment in biometric authentication methods and secure element technologies that protect consumer data while simplifying the checkout process for retailers and service providers alike.

Top Strategies Used by Key Market Participants

Key players in the Europe digital payment market primarily employ mergers and acquisitions to rapidly expand their service portfolios and enter new geographic territories without building infrastructure from scratch. Companies frequently pursue strategic partnerships with fintech startups to integrate innovative technologies such as blockchain and artificial intelligence into their existing platforms. Another dominant strategy involves heavy investment in research and development to create proprietary fraud detection algorithms and enhance security protocols against evolving cyber threats. Market participants also focus on developing omnichannel solutions that seamlessly unify online and offline payment experiences for merchants and consumers. Furthermore, firms actively collaborate with regulatory bodies to ensure compliance with changing laws while shaping future policies that favor digital adoption. Expanding into embedded finance allows these entities to embed payment capabilities directly into non-financial software ecosystems thereby capturing new revenue streams and increasing customer stickiness across various industry verticals.

MARKET SEGMENTATION

This research report on the European digital payment market has been segmented and sub-segmented based on categories.

By Component

By Deployment Model

By Organization Size

- Small and Medium Enterprise

- Large Enterprise

By Vertical

- BFSI

- IT Telecommunication

- Retail E commerce

- Hospitality

- Healthcare

- Media Entertainment

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe