The Drone Industry Could Double Over the Next Decade

Is it possible that the drone industry could double over the next decade? According to the Global Drone Market Report 2026-2035 from German-based industry group Drone Industry Insights, it very well could.

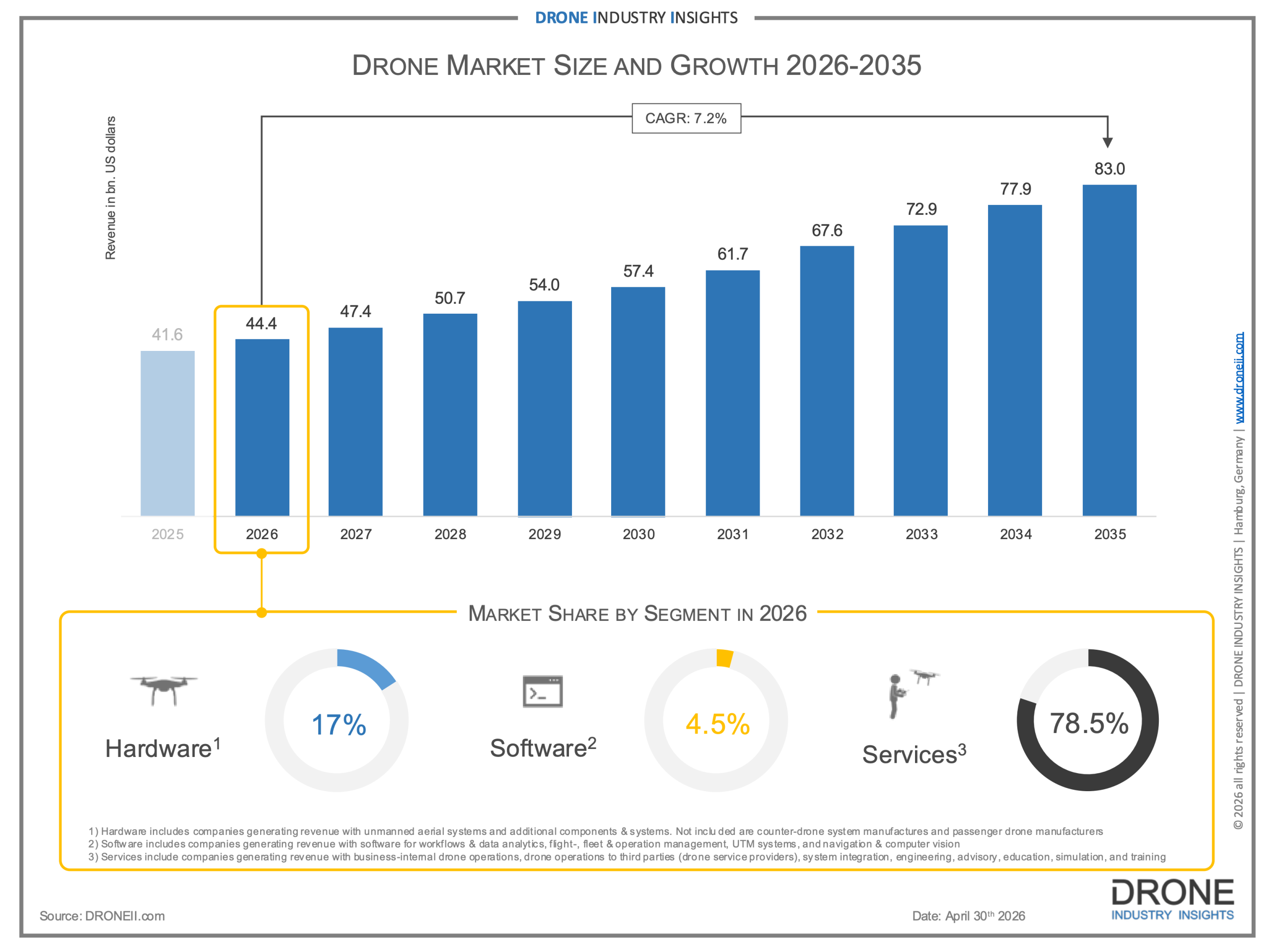

DII’s report suggests the civil drone market is projected to grow from $44.4 billion in 2026 to $83 billion by 2035. That’s a compound annual growth rate of 7.2% sustained over ten years, across commercial, recreational and dual-use applications. That means the drone industry would be roughly on track to nearly double in size over the next decade.

But while that trajectory is credible, it’s also not guaranteed. Here’s what the data says, what it doesn’t say, and what the next ten years actually look like from where we’re standing.

A funding reversal after the post-COVID decline

Drone investment declined 42% in 2023 and another 52% in 2024, marking a brutal two-year correction that forced consolidation, layoffs, and strategic pivots across the industry. But things are looking up, particularly given how 2025 saw a dramatic reversal. Total drone funding in 2025 reached $3.86 billion, surpassing the previous record of $3.67 billion set in 2021.

But it’s also important to understand the composition of that investment. Approximately 77% of the total went to dual-use drone companies (a fancy term for companies serving both civilian and defense markets). The purely commercial drone market raised $888 million, which — while more than double the 2024 total — represented only 23% of overall funding.

It’s also important to read that alongside the broader market context. U.S. stocks as a whole are at or near all-time highs in 2026. Meanwhile, defense spending is surging globally, driven by the Ukraine war, the Iran conflict, and a broader rearmament trend across NATO allies and the Indo-Pacific. The current drone industry is benefiting from that macro tailwind in ways that are specific to the current geopolitical moment.

So will those tailwinds fully persist? For what it’s worth, approximately $1.7 billion was invested in just the first two months of 2026, with capital flowing into both purely civilian applications and dual-use, suggesting that the recovery has legs beyond defense spending alone.

Where the money is actually going in drones

Hardware

Hardware companies attracted 77% of 2025 investment, marking a significant reversal from the software-first trend of previous years.

Why? I largely attribute this to the policy environment, which has made supply chain sovereignty a strategic priority. The FCC’s foreign drone ban, the NDAA restrictions on Chinese-manufactured components, as well as the Blue UAS program’s requirements for domestic supply chains create demand for American-made drones that didn’t exist at this scale even a few years ago years ago.

That’s led to major investments including Skydio’s $3.5 billion domestic manufacturing commitment.

Drone service providers

DII’s 2026 market breakdown shows services accounting for 78.5% of the civil drone market. Meanwhile, hardware accounts for 17% and software accounts for 4.5%.

This covers not just training or flights done for you, but has extend recently to even more flexible products like AirData’s public safety program, where agencies subscribe to fleet intelligence rather than buying fleet management software. There’s also Lucid Bots’ Lucid Refresh subscription model, where operators subscribe to a drone cleaning rental service rather than buying hardware outright.

How are commercial drones actually being used in 2026?

According to DII, construction is the largest vertical for commercial drone use in 2026, with energy and agriculture close behind. Inspection (which encompasses pipelines, power lines, wind turbines, offshore platforms and refineries) remains the dominant commercial use case.

Mapping and surveying also continue to lead. And despite persistent regulatory headwinds, drone delivery is still growing — healthcare delivery (medical samples, vaccines, defibrillators) leading the way, with logistics and food delivery behind it. Between Flytrex’s new Sky2 drone capable of delivering two large pizzas in a single flight and Matternet’s NHS operations in Central London, we’re still seeing examples of drone delivery growth.

What about the recreational market for drones?

The rate of people looking for toy drones is dwindling — and DII’s report affirms that the recreational segment is contributing little to overall market growth.

The FCC’s foreign drone ban may accelerate that stagnation, as removing DJI from the U.S. consumer market without a domestic alternative at equivalent price and capability creates a barrier to entry for new recreational pilots that didn’t exist two years ago.

What challenges to expect in the years ahead

Inflation is a real constraint. The DII report notes rising price sensitivity as a persistent challenge for drone companies seeking to scale. After several years of elevated inflation in the U.S. and Europe, enterprise customers are scrutinizing ROI more carefully than they were in the easy-money environment of 2020-2021.

To succeed over the next decade, drone service providers need to demonstrate clear, quantifiable value rather than selling on novelty or future potential. The companies that have built rigorous ROI frameworks — Lucid Bots’ data showing average revenue of $14,023 per commercial cleaning job, for example — are better positioned than those still selling on vision.

Regulatory progress is uncertain. BVLOS authorization at scale (meaning the ability for commercial operators to fly drones beyond visual line of sight routinely rather than just under individual waivers) is the single biggest unlock for applications such as drone delivery, infrastructure inspection, and agricultural applications.

Part 108 — the anticipated regulatory framework for one-to-many operations — is key in that progress, though final rules are still pending.

The next decade will be defined by which of those variables resolve in the industry’s favor, and how quickly. The technology is largely ready and drone investment is finally returning. The policy environment is the primary variable that the industry can influence but not control. Drone companies that build accordingly are the ones most likely to be standing when the decade closes.

Want more? Check out the report from Drone Industry Insights.

Related

Discover more from The Drone Girl

Subscribe to get the latest posts sent to your email.