Europe Online Learning Market Size, Share & Analysis, 2034

Europe Online Learning Market Report Summary

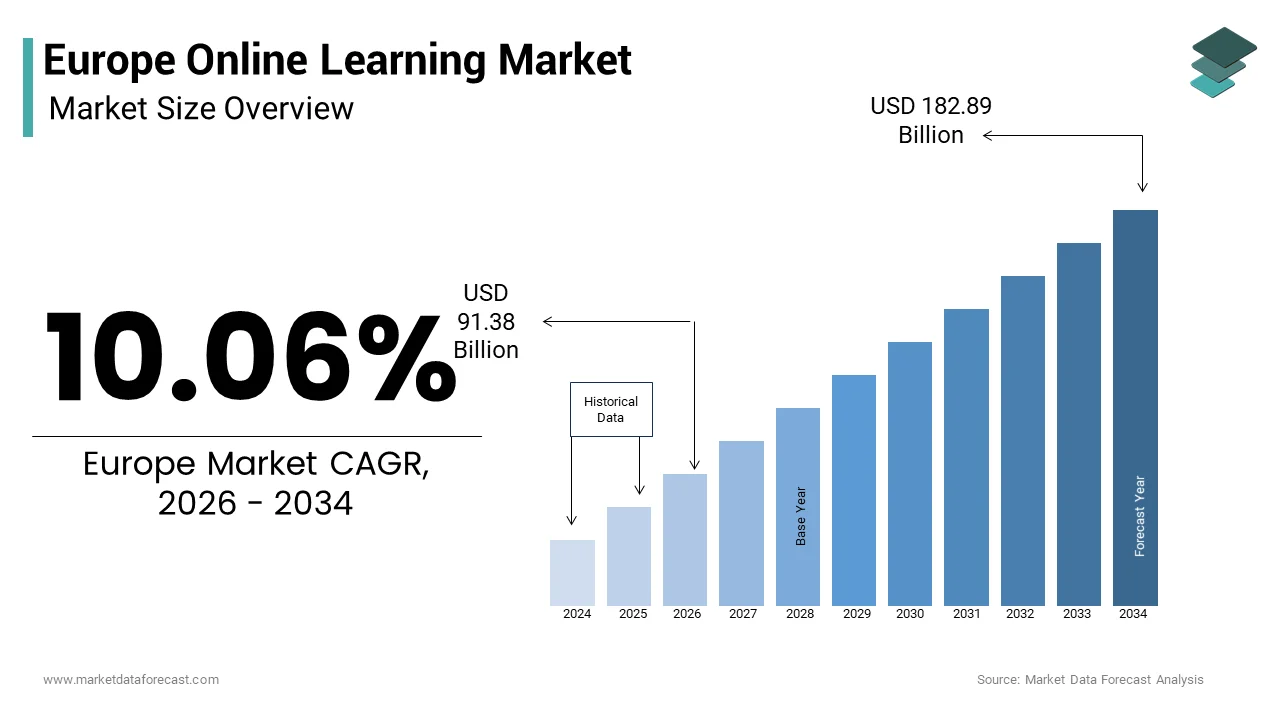

The Europe online learning market was valued at USD 83.02 billion in 2025, is estimated to reach USD 91.38 billion in 2026, and is projected to grow to USD 182.89 billion by 2034, expanding at a CAGR of 10.06% during the forecast period from 2026 to 2034. The growth of the market is driven by the increasing adoption of digital education platforms, rising demand for flexible learning solutions, and the growing integration of advanced technologies in education and corporate training. The widespread availability of high-speed internet, growing use of mobile devices, and the increasing demand for continuous professional development are further supporting the expansion of online learning across Europe. Additionally, government initiatives promoting digital education and the rapid adoption of hybrid learning models by universities and enterprises are accelerating the market growth.

Key Market Trends

- Rising adoption of self-paced learning programs that allow learners to access educational content anytime and anywhere, improving flexibility and convenience.

- Increasing integration of advanced technologies such as artificial intelligence, analytics, and adaptive learning systems to personalize educational experiences.

- Growing demand for corporate training and upskilling programs as organizations focus on workforce development in the digital economy.

- Expansion of mobile learning and cloud-based learning platforms that enable seamless access to courses across multiple devices.

- Increasing partnerships between educational institutions and digital learning platforms to deliver certified online programs and professional courses.

Segmental Insights

- Based on delivery mode, the self-paced learning segment held the largest share of 63.1% of the Europe online learning market in 2025. The dominance of this segment is attributed to the flexibility it offers learners to study at their own pace, making it particularly attractive for working professionals and students seeking personalized learning schedules.

- Based on technology, the learning management systems (LMS) segment dominated the market and captured a 55.7% share in 2025. Learning management systems are widely adopted by educational institutions and enterprises to manage, deliver, and track digital learning programs efficiently.

- Based on end-user, the academic segment accounted for the largest share of 48.2% of the Europe online learning market in 2025. The increasing digitalization of schools and universities, along with the growing adoption of blended and hybrid learning models, is driving strong demand for online learning solutions in the academic sector.

Regional Insights

The European online learning market is experiencing strong growth across major economies as digital education becomes increasingly important for both academic institutions and corporate organizations.

- Germany led the European online learning market and accounted for 24.8% of the market share in 2025, supported by strong investments in digital education infrastructure and increasing demand for corporate e-learning programs.

- The United Kingdom was the second-largest market, capturing 19.3% of the market share in 2025, driven by the rapid adoption of online education platforms, a strong ed-tech ecosystem, and increasing partnerships between universities and digital learning providers.

- France is emerging as a key contributor to the European online learning market due to government initiatives aimed at digitizing the national education system and encouraging lifelong learning programs.

- Italy continues to witness steady growth as the country leverages its strong academic heritage and expanding technology sector to support the adoption of digital learning platforms across universities and professional training institutions.

- Spain is anticipated to experience notable growth during the forecast period owing to increasing investments in digital education infrastructure and rising demand for flexible learning solutions among students and working professionals.

Competitive Landscape

The Europe online learning market is highly competitive and characterized by the presence of global ed-tech companies and specialized learning platform providers. Market players are focusing on expanding their course offerings, integrating advanced learning technologies, and forming strategic partnerships with universities and enterprises to strengthen their market presence. Additionally, companies are investing in artificial intelligence-driven learning platforms, personalized course recommendations, and mobile-based learning solutions to enhance user engagement and learning outcomes.

Prominent players in the Europe online learning market include Coursera Inc., Udemy Inc., LinkedIn Learning, edX (2U Inc.), Skillsoft, Pluralsight, Blackboard Inc., Instructure (Canvas), Cornerstone OnDemand, Moodle, Docebo S.p.A., Pearson plc, SAP Litmos, G-Cube, Chegg Inc., Udacity, D2L Corp. (Brightspace), Google LLC (Classroom), Aptara, and FutureLearn Ltd.

Europe Online Learning Market Size

The Europe online learning market size was valued at USD 83.02 billion in 2025 and is anticipated to reach USD 91.38 billion by 2026 to reach from USD 182.89 billion by 2034, growing at a CAGR of 10.06% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Online Learning Market

Online learning is a flexible, internet-based education method where students access, study, and complete coursework, degrees, or training remotely via digital platforms, bypassing the need for physical classrooms. This sector has evolved from static digitized textbooks to dynamic adaptive learning environments utilizing artificial intelligence for personalized curriculum paths and real-time performance analytics. The fundamental shift in pedagogical approaches defines the current landscape as traditional institutions increasingly blend physical attendance with remote learning modules to enhance flexibility and reach. As per sources, the share of individuals with at least basic digital skills in the European Union is steadily increasing, though significant disparities remain between age groups and across different regions. The penetration of high speed broadband infrastructure supports this growth. Access to high-speed internet in European households is growing, particularly in urban areas, with a major push towards full connectivity by 2030. Literacy rates remain exceptionally high. The Organisation for Economic Co-operation and Development noting that average reading scores in Europe consistently rank among the top globally fostering a culture receptive to continuous learning. The regulatory environment shaped by the European Education Area initiative influences how qualifications are recognized across borders making standardization a central operational requirement. This market functions as a critical engine for workforce reskilling while enabling students in remote regions to access premium educational resources previously unavailable locally.

PRIMARY DEMAND DRIVERS

Urgent Need for Workforce Reskilling Drives Corporate Adoption

Technological disruption and automation are moving at a rapid pace across European industries, which drives the growth of the Europe online learning market. This acts as a trigger for the surge in corporate investment in online upskilling and reskilling programs. Companies increasingly recognize that traditional hiring cannot keep up with the demand for digital competencies forcing them to train existing employees through flexible online platforms. European employers are increasingly struggling to find workers with suitable skills, causing a greater reliance on internal training and in-house development. The proliferation of artificial intelligence and green technologies requires continuous learning cycles that only on-demand digital education can efficiently provide without disrupting daily operations. The rapid acceleration of digital and green transitions is requiring a significant portion of the European workforce to participate in continuous learning and skill adaptation. This urgency drives demand for micro-credentials and nano-degrees that offer quick validation of specific skills rather than lengthy traditional degrees. Industries such as finance healthcare and manufacturing are leading this charge by partnering with ed-tech firms to create customized learning portals. The ability to track progress and measure skill acquisition through analytics makes online education attractive to human resource departments seeking measurable returns on training investments. As the skills gap widens the dependency on scalable digital learning solutions becomes absolute for business survival. This structural change in workforce development guarantees that corporate online education will remain a dominant growth engine.

Expansion of Higher Education Accessibility Fuels Student Enrollment

Digital channels are democratizing higher education, which further contributes to the expansion of the Europe online learning market. This shift is a primary demand driver, compelling universities and colleges to expand their online course offerings for broader demographics. Physical campus capacities are facing limitations as tuition costs continue to rise. Consequently, students are increasingly seeking affordable and flexible alternatives that allow them to balance study with work or family commitments. European higher education institutions have fundamentally integrated digital, online, and hybrid learning into their curriculum, making it a standard component of higher education delivery. The removal of geographical barriers enables students from rural areas or smaller nations to access prestigious programs offered by top universities in major hubs without relocation costs. Participation in adult learning and lifelong learning initiatives is rising in Europe, with digital and online platforms playing a significant role in providing new training opportunities. The rise of Massive Open Online Courses has further intensified interest by providing free or low-cost entry points to specialized knowledge attracting lifelong learners. Governments are actively supporting this trend through funding initiatives that subsidize digital infrastructure for public universities ensuring equitable access. The flexibility of asynchronous learning appeals strongly to non-traditional students including working professionals and parents who require adaptable schedules. Consequently, the health of the online learning market is inextricably linked to the strategic priorities of higher education providers to remain competitive and inclusive.

CRITICAL MARKET RESTRAINTS

Digital Divide and Infrastructure Disparities Limit Reach

A persistent gap in digital infrastructure and device availability exists across different European regions, and thereby stunts the growth of the Europe online learning market. This disparity restricts access to high-quality online education for disadvantaged populations. Urban centers enjoy robust connectivity. In contrast, rural areas and lower-income households often struggle with unreliable internet speeds and a lack of suitable hardware for effective learning. As per research, internet access is widely available across Europe, though connectivity challenges and lower usage rates persist in specific, more rural or less developed regions. This infrastructural inequality forces educators to dilute content quality to accommodate slower connections thereby reducing the effectiveness of interactive and immersive learning tools. Students from disadvantaged economic backgrounds frequently experience restricted educational opportunities due to a reliance on mobile devices instead of dedicated computers for academic work. The fragmentation of digital readiness across member states adds complexity for pan-European educational initiatives requiring tailored solutions for different connectivity levels. Institutions now face higher costs to provide offline materials or loaner devices to ensure inclusivity which strains already tight budgets. The inability to guarantee equal access undermines the core promise of online education as a democratizing force and limits the total addressable market. The sector continues to grapple with balancing advanced technological integration against the fundamental reality of uneven digital access mandated by socioeconomic disparities.

Lack of Standardized Accreditation Hinders Credential Recognition

The lack of a unified European framework for accrediting online qualifications is a major obstacle to the Europe online learning market. This gap leads to significant hesitation among learners and employers concerning the legitimacy of digital degrees. When certificates from online platforms are not universally accepted or understood it diminishes their utility in the labor market and discourages enrollment in non-traditional programs. According to the European Network of Information Centres significant variations exist in how different countries evaluate and accept online credits leading to confusion and administrative bottlenecks for mobile students. This regulatory ambiguity leads to a perception that online qualifications are inferior to traditional campus-based degrees despite similar curriculum rigor. Major employers which form the bulk of the demand for skilled labor are particularly cautious and may prioritize candidates with conventional credentials due to familiarity and trust. Data from the European Quality Assurance Register indicates that only a fraction of online programs have undergone cross-border quality assurance processes limiting their portability. The volatility makes it difficult for ed-tech providers to market their courses effectively across borders as they must navigate distinct national accreditation bodies. Furthermore the fluctuating recognition standards impact the willingness of students to invest time and money in programs that may not yield career advancement. This macro-regulatory headwind creates a cautious environment where innovation in credentialing stagnates despite the underlying demand for flexible education pathways.

EMERGING GROWTH OPPORTUNITIES

Integration of Artificial Intelligence Enables Hyper-Personalization

Artificial intelligence and machine learning are being rapidly adopted, which creates many new growth options for education providers and for the Europe online learning market. This technology allows for hyper-personalized learning experiences that adapt to student needs in real time. Learners now expect tailored content. Consequently, AI algorithms analyze performance data to adjust difficulty, suggest resources, and predict potential struggles. European schools are increasingly exploring AI integration, with a focus on ethical frameworks and pilot programs, particularly regarding generative AI in schools. This transition allows platforms to create dynamic curricula that evolve with the student significantly improving engagement and retention rates compared to static one-size-fits-all models. The ability to provide instant feedback and customized learning paths enhances the relevance of education and improves outcomes for students with varying abilities. Data-driven innovation is rising, with significant growth in AI infrastructure investment across various European sectors to improve decision-making and operational efficiency. Providers are increasingly allocating portions of their development budgets to these digital channels to capture deeper insights into learner behavior. The format supports adaptive testing environments that reduce anxiety and provide accurate assessments of competency bridging the gap between teaching and evaluation. As algorithms become more sophisticated the barrier to entry for high-quality personalized tutoring lowers enabling scalable solutions for mass education. This technological leap ensures that the European market remains at the forefront of educational innovation driving efficiency and effectiveness across all verticals.

Rise of Micro-Credentials Addresses Specific Skill Gaps

The growing demand for short-term targeted learning modules, known as micro-credentials, offers a potential opportunity for online education providers and for the Europe online learning market expansion. This allows them to address specific skill gaps rapidly without requiring long-term degree commitments. These compact certifications allow professionals to upskill in niche areas such as data analytics cybersecurity or sustainable management aligning directly with immediate labor market needs. There is a significant, growing interest among European adults in upskilling and reskilling to address skill shortages and enhance employability through flexible, short-term training. This transition allows learners to stack multiple credentials over time to build comprehensive qualifications offering flexibility that traditional degrees cannot match. The ability to earn recognized badges quickly enhances career mobility and provides tangible proof of competency to potential employers. Employers are increasingly recognizing the value of micro-credentials for specific skillsets, particularly in tech and rapidly evolving sectors, often using them to complement rather than replace traditional degrees. Providers are increasingly collaborating with industry leaders to design curricula that ensure immediate relevance and job readiness. The format supports just-in-time learning allowing individuals to acquire skills exactly when needed for project work or promotion. As the pace of technological change accelerates the inventory of required micro-skills will grow substantially. This evolution represents a paradigm shift where education becomes a continuous lifelong process rather than a one-time event opening new revenue streams.

PERSISTENT MARKET CHALLENGES

Ensuring Academic Integrity in Remote Assessments

Maintaining academic integrity during remote examinations is a pervasive challenge to the Europe online learning market. It creates a significant hurdle by undermining the credibility of digital qualifications. The ease with which students can access unauthorized resources or collaborate illicitly during online tests makes verification difficult and costly for institutions. Online assessments present a higher risk for academic misconduct compared to in-person exams, leading to increased efforts by quality assurance agencies to secure them. Institutions often struggle with the ethical implications and privacy concerns associated with proctoring software that monitors students via webcams and screen sharing. The lack of standardized protocols for remote invigilation means that policies vary widely across universities diluting the perceived fairness of the system. Cross-border enforcement issues remain problematic especially when students reside in jurisdictions with different data protection laws limiting the use of monitoring tools. Many students feel that online proctoring software invades their privacy, leading to widespread resistance to strict remote monitoring and demands for more data-secure assessment methods. This fragmentation increases the cost and complexity of administering secure assessments requiring specialized technology and legal oversight. The inability to guarantee exam security accurately undermines confidence in online degrees and hampers wider acceptance by employers. Overcoming this disjointed landscape requires substantial investment in secure assessment technologies and harmonized ethical guidelines.

High Dropout Rates Due to Lack of Social Engagement

Online learners are often susceptible to isolation and disengagement, which hinders the expansion of the Europe online learning market. This susceptibility creates intense operational instability for education providers who rely on sustained enrollment and completion rates. Students frequently miss the social interactions and structured environment provided by physical campuses. Without these elements, motivation wanes and dropout rates become significantly higher than in traditional settings. Fully online courses face higher dropout rates and lower completion rates compared to in-person or hybrid alternatives, making retention a significant challenge for institutions. This volatility disproportionately affects self-directed learners who lack the discipline or support networks necessary to navigate independent study effectively. The sheer volume of available content can lead to choice paralysis where students feel overwhelmed and abandon their studies before finishing. Providers continuously update their platforms to include gamification and peer interaction features to combat loneliness but these solutions often fall short of replicating genuine human connection. The competition for attention extends beyond education as work and family obligations frequently take precedence in the home environment. Lead times for degree completion are extending. Institutions must therefore invest more in mentorship programs and community building initiatives to mitigate attrition which further escalates operational budgets. This relentless pressure on retention threatens the financial sustainability and reputation of many online education initiatives.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

10.06% |

|

Segments Covered |

By Delivery Mode, Technology, End-User, and Country |

|

Various Analyses Covered |

Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Coursera Inc., Udemy Inc., LinkedIn Learning, edX (2U Inc.), Skillsoft, Pluralsight, Blackboard Inc., Instructure (Canvas), Cornerstone OnDemand, Moodle, Docebo S.p.A., Pearson plc, SAP Litmos, G-Cube, Chegg Inc., Udacity, D2L Corp. (Brightspace), Google LLC (Classroom), Aptara, FutureLearn Ltd |

SEGMENTAL ANALYSIS

By Delivery Mode Insights

In 2025, the self-paced learning segment held the majority share of 63.1% of the Europe online learning market. The unparalleled flexibility it offers to learners who must balance education with full-time employment or family responsibilities across diverse time zones drives the supremacy of the segment. The main thing pushing this is the asynchronous nature of the content which allows individuals to access materials at any hour without coordinating schedules with instructors or peers. Adult learners in Europe increasingly favor flexible, digital, and on-demand learning formats that accommodate working schedules, notes the European Association of Distance Teaching Universities. The ability to pause rewind and review complex concepts multiple times enhances comprehension and retention rates particularly for difficult technical subjects. The OECD notes that strengthening online course design, user experience, and mobile accessibility is essential for improving learner engagement and completion rates. Institutions favor this model because it reduces the logistical complexity of scheduling live sessions across different geographical locations for international cohorts. The scalability of self-paced content means that a single course can serve thousands of students simultaneously without additional instructor overhead. These dynamics solidify self-paced learning as the bedrock of the online education industry.

The instructor-led training segment is predicted to witness the highest CAGR of 18.3% from 2026 to 2034 due to the increasing demand for real-time interaction immediate feedback and social accountability which mimics the traditional classroom experience more closely than self-study methods. The engine behind this expansion is the advancement of low-latency video conferencing technologies that enable seamless live collaboration and instant question and answer sessions between educators and students. The European University Association observes that higher education institutions are increasingly integrating digital transformation, seeking to balance flexible online options with structured, interactive learning experiences. The rise of hybrid learning models where physical classrooms are extended digitally requires robust synchronous tools to include remote participants fully in real-time discussions. Studies indicate that interactive live virtual sessions often foster higher immediate behavioral engagement, whereas self-paced modules are better suited for individual flexibility and independent study. Interactive features such as live polling breakout rooms and shared whiteboards enhance the dynamism of lessons making them more engaging for digital natives. Employers also value synchronous training for soft skills development where role-playing and immediate coaching are essential. The integration of artificial intelligence to provide real-time transcription and translation further breaks down language barriers in multinational cohorts. This alignment with the human need for connection ensures the instructor-led segment will experience sustained double-digit growth.

By Technology Insights

The learning management systems segment dominated the Europe online learning market and captured a 55.7% share in 2025. The dominance of the segment is driven by the critical need for centralized platforms that manage user enrollment content delivery assessment and reporting within a single secure environment. A key pillar of market growth is the widespread adoption of these systems by both educational institutions and corporations to streamline administrative workflows and ensure compliance with data protection regulations. Higher education institutions across Europe are accelerating the transition to cloud-based, remote-accessible, and interoperable digital platforms. The scalability of LMS solutions enables providers to update content instantly ensuring that learners always access the most current information without physical redistribution costs. Educational software spending in Western Europe is growing, driven by a strong demand for personalized learning and AI-driven adaptive functionalities. Institutions favor LMS because it reduces long-term operational expenses associated with manual grading and record keeping while offering rich multimedia experiences that static materials cannot match. The integration of analytics tools within these platforms empowers educators to identify at-risk students early and intervene proactively. Furthermore the ability to integrate third-party tools such as video conferencing and plagiarism detection creates a comprehensive ecosystem that locks in user dependency. These structural advantages ensure that LMS remains the backbone of the digital education landscape.

The artificial intelligence powered adaptive learning segment is estimated to register the fastest CAGR of 24.7% during the forecast period owing to the increasing sophistication of AI algorithms that offer capabilities impossible to replicate in standard static content delivery setups. Apart from these, a primary driver is the urgent need for educational institutions to provide hyper-personalized learning paths that adjust difficulty levels and suggest resources based on individual student performance in real time. The adoption of AI-driven tools in European education is growing rapidly, accelerated by the need for personalized learning in flexible, hybrid, and remote environments. The rise of predictive analytics allows platforms to anticipate learner struggles before failure occurs enabling timely interventions that significantly improve success rates. European organizations are increasingly investing in AI and machine learning tools, with a growing focus on optimizing student engagement and pedagogical outcomes through data analytics. Providers are continuously enhancing natural language processing features to facilitate automated essay grading and conversational tutoring thereby alleviating teacher workload. The ability to rapidly deploy personalized curricula gives users a significant competitive advantage in skill acquisition. Computing costs are declining, and algorithmic accuracy is improving. Consequently, even conservative institutions are accelerating their adoption plans. This convergence of technological capability and pedagogical efficacy ensures the AI segment will maintain its rapid growth trajectory.

By End-User Insights

The academic segment was the largest segment in the Europe online learning market and occupied a 48.2% share in 2025. The prominence of the segment is credited to the massive scale of student populations in universities and schools who require digital tools for curriculum delivery and administrative management. An additional accelerator is the strategic pivot of higher education institutions toward hybrid and fully online degree programs to attract international students and non-traditional learners. European higher education institutions are increasingly, if not universally, adopting and integrating digital learning platforms as a standard component of education rather than just a contingency tool. The removal of geographical barriers enables universities to tap into vast international markets generating significant new revenue streams without expanding physical campus infrastructure. Cross-border online education is experiencing a sustained rise, moving from a temporary pandemic measure to a long-term strategic model for institutions, as observed in global EdTech and OECD analyses. The flexibility of online schedules appeals strongly to working professionals seeking advanced degrees while maintaining full-time employment. Governments are actively supporting this trend through funding initiatives that subsidize digital transformation projects in public universities. The integration of virtual laboratories and simulation tools now allows for rigorous practical training in fields like medicine and engineering remotely. This convergence of institutional strategy and learner demand ensures the academic sector remains the primary revenue engine for the online learning industry.

The corporate segment is anticipated to witness the fastest CAGR of 19.6% over the forecast period. This swift growth is propelled by the critical need for continuous workforce upskilling and reskilling to keep pace with rapid technological advancements and regulatory changes. The primary factor driving this growth is the cost-effectiveness and scalability of online training programs which allow multinational corporations to standardize learning across diverse geographic locations without travel expenses. Corporate training in Europe is rapidly shifting toward digitalization to address skill shortages and enhance workforce adaptability, particularly through virtual training modules. The ability to track individual progress and measure skill acquisition through detailed analytics makes online education highly attractive to human resource departments seeking measurable returns on investment. Corporate spending on e-learning is increasing, driven by the need for cost-effective, scalable, and personalized training solutions, frequently replacing traditional, in-person, and expensive workshops. Micro-learning modules delivered via mobile devices enable employees to learn during workflow interruptions maximizing productivity and minimizing downtime. The customization of content to address specific organizational challenges ensures relevance and higher engagement levels among staff. Furthermore the agility of online platforms allows companies to roll out new policy training or product knowledge updates instantly across the entire enterprise. These structural advantages ensure that the corporate sector will outpace all other end users in growth velocity.

COUNTRY LEVEL ANALYSIS

Germany Online Learning Market Analysis

Germany led the European online learning market and accounted for a 24.8% share in 2025. The leading position of the German market is supported by its robust industrial base and strong tradition of vocational training which is rapidly digitizing to meet Industry 4.0 requirements. A further key driver of this dominance is the dual education system where companies and schools collaborate closely to deliver blended learning programs that combine theoretical online modules with practical apprenticeships. There is a strong, consistent upward trend in internet penetration across Germany, with nearly all citizens accessing the internet for various purposes, including learning. The country serves as a testing ground for advanced technologies such as virtual reality simulations for technical training which are widely adopted by manufacturing giants. A well-developed broadband infrastructure ensures that even rural vocational centers can access high-quality digital content seamlessly. Germany is experiencing increased government-supported investment in digital infrastructure and tools for education and training. The presence of major ed-tech startups and established publishing houses who have aggressively digitized their curricula contributes significantly to the depth of available content. Strict data protection standards have forced platforms to build trust through transparency enhancing long-term adoption rates. This combination of economic strength cultural appreciation for lifelong learning and technological readiness ensures Germany retains its top rank.

United Kingdom Online Learning Market Analysis

The United Kingdom was the second largest country in the Europe online learning market and captured a 19.3% share in 2025. The expansion of the UK market is fuelled by its world-renowned higher education institutions and mature ed-tech ecosystem. The nation benefits from being a global hub for English-language content which attracts millions of international students to its online programs. A top reason for market improvement is the proactive stance of UK universities in launching fully online degrees that rival their on-campus counterparts in prestige and rigor. The UK has seen a robust increase in total higher education enrollments over recent years, though growth rates fluctuate depending on the specific mode of study and international student intake. The presence of leading venture capital firms fosters a vibrant startup scene that continuously innovates in areas like adaptive learning and AI tutoring. Overseas demand for British higher education, including digital and distance learning models, remains high, creating significant export potential for UK educational institutions. The post-Brexit regulatory environment has encouraged institutions to diversify revenue streams through global online offerings reducing reliance on domestic tuition fees. High digital literacy rates among the population facilitate rapid adoption of new learning platforms across all age groups. The strength of the English language content market also allows UK-based providers to serve as hubs for expansion into North America and Asia. This blend of academic excellence entrepreneurial spirit and global reach cements the UK as a pivotal market.

France Online Learning Market Analysis

France is another key player in the Europe online learning market due to aggressive government initiatives to digitize the national education system and promote lifelong learning. The market status shows that strong state involvement in developing public platforms and subsidizing access to digital resources for students and workers alike. Among these, a major driving factor is the “France 2030” investment plan which allocates billions of euros to transform education through technology and reduce inequalities in access. French schools are expanding the use of digital tools and resources in classrooms, supported by national strategies to integrate technology into teaching. The popularity of MOOCs hosted by prestigious institutions like Sorbonne University drives significant traffic to national platforms during academic terms. There is a significant focus on digital upskilling and expanding vocational training, with increased use of CPF funding for professional development. The existence of strong labor unions that negotiate digital training rights for employees adds a unique dynamic to the corporate learning segment. Cross-border collaborations within the EU allow French learners to access a wider range of international titles seamlessly. The focus on protecting French language content ensures that local providers thrive alongside global giants. This strategic balance between state support and market innovation ensures France remains a key growth engine.

Italy Online Learning Market Analysis

Italy maintains a significant position in the European online learning market. The country leverages its rich academic heritage and growing tech sector to sustain steady demand for both academic and professional digital learning solutions. The market status is defined by a rapid catch-up in digital adoption as traditional institutions increasingly recognize the necessity of online channels to reach broader demographics. Internet access in Italian families is steadily growing, with a high proportion of households having broadband connectivity. A key driving factor is the government’s National Recovery and Resilience Plan which includes substantial funding for digitalizing schools and universities to modernize the education infrastructure. The tourism and hospitality sectors contribute significantly to demand for specialized online training programs to upskill workers in these vital industries. Digital learning is accelerating in Italy, with a strong focus on AI-driven platforms and increased use of mobile devices for education. The fragmented nature of the small business landscape creates opportunities for scalable online training solutions that offer cost-effective compliance and skills development. The fusion of cultural wealth with modern digital tools positions Italy for sustained growth as connectivity improves in the south.

Spain Online Learning Market Analysis

Spain is anticipated to grow in the Europe online learning market during the forecast period owing to its strategic role as a bridge between European and Latin American educational markets. The nation has emerged as a critical hub for Spanish-language digital content serving millions of speakers globally through its online platforms. The market status is characterized by rapid growth in corporate training and language learning sectors as young demographics embrace flexible learning formats. Spain is significantly increasing its digital investment, especially through the SME Digitalization Plan and initiatives aimed at improving educational and professional skills. A primary driving factor is the intense popularity of language learning apps and platforms where Spain serves as a content creation center for global audiences. The government has implemented policies to promote digital literacy and access to culture which has boosted online course consumption in rural areas. Internet use for online learning is growing in Spain, with a substantial portion of users engaging in online courses and accessing educational materials. The rise of university partnerships with Latin American institutions drives cross-border enrollment in joint online degree programs. Urban centers like Madrid and Barcelona are becoming hubs for ed-tech startups attracting talent and investment from across the Spanish-speaking world. This dynamic environment ensures Spain plays an increasingly important role in the regional digital economy.

COMPETITIVE LANDSCAPE

The competition in the Europe online learning market is intensely fierce characterized by a constant battle for learner attention and institutional contracts among global platforms and specialized regional providers. Dominant players leverage vast content libraries and advanced technology to offer superior user experiences that smaller competitors struggle to match without significant investment. However niche operators thrive by focusing on specific industries or local curricula where they can offer tailored expertise and cultural relevance that multinational corporations often lack. The landscape is further complicated by stringent data protection laws and varying accreditation standards across nations which forces all participants to maintain robust compliance frameworks. New entrants from the corporate training and vocational sectors are disrupting traditional models by offering just-in-time learning solutions that align closely with immediate job market needs. Price wars occasionally erupt in subscription fees but differentiation increasingly relies on content quality certification value and learner support services. Mergers and acquisitions remain common as companies seek to consolidate content portfolios and expand their geographic footprint efficiently. This dynamic environment ensures rapid evolution where adaptability technological prowess and pedagogical effectiveness determine long term survival and success.

KEY MARKET PLAYERS

A Dominating players that are in the Europe online learning market are

- Coursera Inc.

- Udemy Inc.

- LinkedIn Learning

- edX (2U Inc.)

- Skillsoft

- Pluralsight

- Blackboard Inc.

- Instructure (Canvas)

- Cornerstone OnDemand

- Moodle

- Docebo S.p.A.

- Pearson plc

- SAP Litmos

- G-Cube

- Chegg Inc.

- Udacity

- D2L Corp. (Brightspace)

- Google LLC (Classroom)

- Aptara

- FutureLearn Ltd

Top Players In The Market

- Coursera operates as a leading global platform connecting learners with universities and companies to offer courses certificates and degrees across Europe. The company leverages partnerships with top European institutions to provide high quality content that meets rigorous academic standards while addressing local skill gaps. Recent actions include expanding its enterprise offerings to help European corporations reskill workforces in artificial intelligence and data science through tailored learning paths. Coursera has launched degree programs specifically designed for the European market ensuring alignment with regional employment needs and regulatory frameworks. The firm continues to invest in mobile accessibility allowing students to learn on the go which is crucial for working professionals. Globally Coursera sets benchmarks for massive open online courses and credential recognition. Their commitment to democratizing education ensures that learners from diverse backgrounds can access world class training without geographical barriers.

- Udemy maintains a massive presence in the Europe online learning market by utilizing an open marketplace model where experts create and sell courses on virtually any topic. The company excels in providing practical skills training ranging from technology and business to personal development which resonates deeply with individual learners and small businesses. Recent strategic moves include enhancing its Udemy Business platform with curated learning collections and analytics tools to help European organizations track employee progress effectively. Udemy has introduced AI driven content recommendations to personalize the learning experience and improve course completion rates significantly. The firm actively develops partnerships with local industry leaders to ensure course content remains relevant to current market demands. Globally Udemy drives innovation in peer-to-peer learning and flexible skill acquisition. Their focus on affordability and breadth of content makes them a preferred choice for lifelong learners seeking immediate application of knowledge.

- SAP SE stands as a dominant force in the European corporate learning sector by integrating education directly into its enterprise resource planning ecosystem. The company offers comprehensive training solutions that help organizations maximize the value of their software investments while upskilling employees in digital transformation technologies. Recent actions involve launching the SAP Learning Hub which provides access to thousands of learning assets including live expert sessions and hands-on practice environments. SAP has expanded its certification programs to cover emerging fields like sustainability management and cloud computing ensuring workforce readiness for future challenges. The firm leverages its extensive customer base across Europe to deliver localized training content in multiple languages. Globally SAP influences corporate education standards by embedding learning into daily workflows. Their dedication to continuous professional development ensures that enterprises can adapt quickly to changing business landscapes and technological advancements.

Top Strategies Used By Key Market Participants

Key players in the Europe online learning market primarily focus on strategic partnerships with accredited universities and industry leaders to enhance content credibility and relevance. Companies heavily invest in artificial intelligence and machine learning to personalize learning paths and provide real-time feedback to students. Major participants are expanding their mobile capabilities to ensure seamless access to educational content across various devices and locations. Development of micro-credentialing and badge systems helps learners demonstrate specific skills to employers effectively. Firms also prioritize data privacy and compliance with European regulations to build trust among users and institutional clients. Continuous localization of content into multiple European languages addresses the diverse linguistic needs of the region. These strategies collectively aim to improve engagement outcomes and scalability while navigating complex regulatory environments.

MARKET SEGMENTATION

This research report on the Europe online learning market is segmented and sub-segmented into the following categories.

By Delivery Mode

- Self-Paced

- Instructor-Led

By Deployment

By Technology

- Online e-learning

- Learning Management System (LMS)

- Mobile e-learning

- Rapid e-learning

- Virtual Classroom

By End-User

- Academic

- Corporate

- Government & Public Sector

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe