Europe Construction Software Market Size, Share & Trends, 2034

Europe Construction Software Market Size

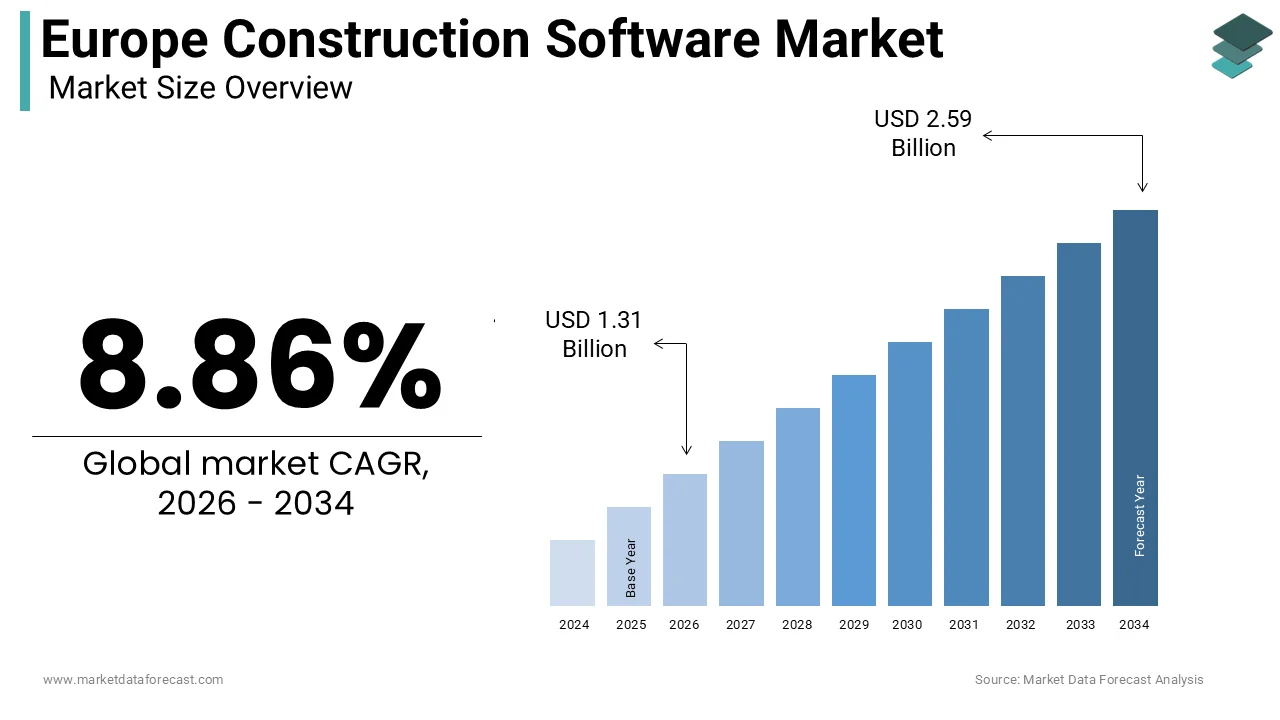

The Europe construction software market size was calculated to be USD 1.20 billion in 2025 and is anticipated to be worth USD 2.59 billion by 2034, from USD 1.31 billion in 2026, growing at a CAGR of 8.86% during the forecast period.

Construction software refers to digital tools and platforms designed specifically to manage, streamline, and automate various stages of construction projects, from initial design and estimation to field operations and final closeout. These technologies include Building Information Modeling project management tools, cost estimation software, and field management applications that facilitate collaboration among architects, engineers, contractors, and clients. The adoption of these digital tools is critical for enhancing productivity, ensuring regulatory compliance, and improving safety standards in an industry traditionally characterized by fragmentation and low digitization. According to Eurostat, the construction sector in the European Union reached a record high of 14.9 million persons employed in late 2025, maintaining its role as a vital pillar for regional job creation. This vast labor force underscores the potential impact of software solutions in optimizing human resource allocation and reducing inefficiencies. As per the European Commission, the narrow construction sector contributes approximately 5.5% of the EU’s total Gross Value Added (GVA), while the broad construction ecosystem, encompassing real estate and engineering, contributes roughly 9% to the total EU GDP. Despite this economic weight, the sector has historically lagged in digital transformation compared to manufacturing or retail. The increasing complexity of modern infrastructure projects, coupled with stringent environmental regulations, necessitates advanced software capabilities for accurate modeling and resource management. The integration of cloud-based platforms enables real-time data sharing, which is essential for coordinating multi-stakeholder projects across different geographical locations. The shift towards modular construction and prefabrication further drives the need for precise digital planning tools. Thus, the market is witnessing a surge in demand for integrated software suites that offer end-to-end visibility from conceptual design to facility management. This digital evolution is pivotal for addressing longstanding challenges such as cost overruns and schedule delays.

MARKET DRIVERS

Government mandates for Building Information Modeling adoption are accelerating digital transformation.

The mandatory implementation of Building Information Modeling by various European governments is a key force behind the growth of the Europe construction software market. Several countries, including the United Kingdom, France, Germany, and the Netherlands, have established clear roadmaps requiring the use of BIM for public sector construction projects. According to the European Commission, the directive on public procurement encourages member states to utilize electronic tools such as BIM for complex construction works to improve transparency and efficiency. This regulatory push forces contractors and consultants to invest in compatible software solutions to remain eligible for lucrative government contracts. As per the UK Government Construction Strategy, the mandate for fully collaborative 3D BIM with all project and asset information documentation and data being electronic was a pivotal moment that significantly increased software penetration in the region. Similar initiatives in Scandinavia and Central Europe are creating a ripple effect where private sector clients also begin to require BIM deliverables to ensure better project outcomes. The standardization of data formats through initiatives like the European Standard EN ISO 19650 further facilitates interoperability between different software platforms. This regulatory environment reduces the risk associated with digital investment as companies know that compliance is not optional but a prerequisite for market participation. The requirement for detailed digital twins of assets at the handover stage also drives the adoption of facility management software. So, software vendors are seeing sustained demand for their products as firms upgrade their technological infrastructure to meet these legal and contractual obligations. This top-down approach ensures a baseline level of digitization across the industry, fostering a more competitive and efficient market landscape.

Urgent need for improved productivity and cost control in a fragmented industry

The persistent issue of low productivity and frequent cost overruns in the regional construction sector is driving the urgent adoption of management and estimation software, which is also a top factor in the expansion of the Europe construction software market. The construction industry in Europe has historically struggled with stagnant productivity growth compared to other sectors, such as manufacturing. According to McKinsey Global Institute, the construction sector’s productivity growth has averaged only 1 percent annually over the past two decades, lagging significantly behind the global economy. This inefficiency results in substantial financial losses, with many projects exceeding their initial budgets and timelines. As per the European Construction Industry Federation, cost overruns and delays are among the most common complaints from clients, leading to strained relationships and reduced profit margins for contractors. Construction software offers solutions to these problems by providing real-time tracking of expenses, resource allocation, and project progress. Cloud-based project management tools enable stakeholders to identify potential bottlenecks early and take corrective actions before they escalate into major issues. The ability to simulate construction processes digitally allows for better planning and risk mitigation, reducing the likelihood of unexpected costs.

Furthermore, automated estimation tools help in creating more accurate bids, thereby improving the chances of winning contracts while maintaining profitability. The integration of artificial intelligence in these software solutions further enhances predictive capabilities, allowing firms to anticipate material price fluctuations and labor shortages. As competition intensifies and margins shrink, construction companies are increasingly viewing software not as a luxury but as a necessity for survival. The drive to optimize operations and enhance profitability is thus a powerful engine for market growth.

MARKET RESTRAINTS

High initial implementation costs and complexity are deterring small and medium enterprises.

The substantial financial burden associated with acquiring and implementing advanced construction software is a major limitation, particularly for small and medium-sized enterprises, which constitute the majority of the European construction market. These companies often operate on thin margins and lack the capital reserves necessary for significant upfront investments in software licenses, hardware, and training. According to the European Commission, small and medium-sized enterprises (SMEs), dominated by micro-firms, account for 99% of all businesses in the EU construction sector, making their financial constraints a critical market factor. The cost of subscription fees for premium software suites can be prohibitive for smaller firms that may only engage in occasional large-scale projects. As per the European Small Business Portal, many small construction firms cite high costs as the primary barrier to digital adoption, fearing that the return on investment will not be realized in the short term. Additionally, the complexity of integrating new software with existing legacy systems requires specialized IT expertise, which these firms often do not possess in-house. The need for continuous training and support further adds to the total cost of ownership. Many smaller contractors rely on informal methods and basic tools that, while inefficient, are familiar and free to use. The perceived risk of disrupting ongoing operations during the transition phase also discourages adoption. Without targeted financial incentives or simplified, affordable solutions tailored to their needs, a large segment of the market remains hesitant to embrace digital transformation. This resistance slows down the overall market penetration rate and limits the potential user base for software vendors.

Resistance to cultural change and a lack of digital skills in the workforce

The deeply ingrained traditional culture of the construction industry, combined with a shortage of digital skills among the workforce, is a formidable restraint to the adoption of new software solutions and thereby negatively impacts the expansion of the Europe construction software market. The construction sector in Europe is characterized by an aging workforce and a reliance on established manual processes that have been used for decades. According to Eurostat and sectoral analyses, the average age of workers in the construction sector remains high, with a significant proportion nearing retirement age and a lack of younger workers entering the field to replace them. This demographic reality means that many experienced professionals are less comfortable with digital tools and may resist changing their working habits. As per the European Centre for the Development of Vocational Training, there is a notable skills gap in digital competencies within the vocational education and training systems for construction trades. Many workers lack the necessary training to effectively use complex software applications, leading to frustration and underutilization of the technology. The industry’s fragmented nature with numerous subcontractors and temporary workers further complicates the standardization of digital processes. Convincing diverse teams to adopt a unified software platform requires significant change management effort,s which many firms are ill-equipped to handle. The fear of job displacement due to automation also contributes to resistance among workers. Without a concerted effort to upskill the workforce and foster a culture of innovation, the full potential of construction software cannot be realized. This cultural inertia slows down the pace of adoption and limits the effectiveness of implemented solutions.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning for predictive analytics

The incorporation of Artificial Intelligence and Machine Learning into this domain paves the way for enhancing decision-making and operational efficiency across the European construction software market. These technologies enable the analysis of vast amounts of historical and real-time data to predict outcomes, identify risks, and optimize resources. According to the European Commission, the application of AI in industrial sectors is expected to grow significantly, offering transformative potential for productivity and safety through initiatives like the Apply AI Strategy. In construction, AI algorithms can analyze project data to forecast potential delays, cost overruns, or safety hazards, allowing managers to take proactive measures. As per the McKinsey Global Institute, AI and automation have the potential to increase productivity in the construction sector significantly, with generative AI alone contributing up to 0.6 percent annually to labor productivity growth through 2040. Software vendors are increasingly embedding AI capabilities into their platforms to offer features such as automated scheduling, risk assessment, and quality control. The ability to process data from drone sensors and Internet of Things devices in real time provides unprecedented visibility into site conditions. This data-driven approach enables more accurate bidding and improved project control.

Furthermore, AI-powered design tools can generate optimized building models that reduce material waste and energy consumption, aligning with sustainability goals. The growing availability of cloud computing power makes these advanced analytics accessible to a broader range of users. Companies that successfully leverage AI can differentiate themselves by offering superior insights and value to their clients. The potential for continuous learning and improvement through machine learning models ensures that the software becomes more effective over time. This technological evolution opens new revenue streams for software providers and creates a competitive advantage for early adopters.

Expansion of Green Building and Sustainability Compliance Tools

The increasing emphasis on sustainability and green building practices in the region creates a significant opportunity for developers of digital tools and platforms in the European construction software market. This enables the developers to offer specialized compliance and optimization tools. The European Green Deal and related regulations, such as the Energy Performance of Buildings Directive, mandate strict energy efficiency standards for new and renovated buildings. According to the European Commission, buildings are responsible for 42 percent of energy consumption and 33 percent of energy-related greenhouse gas emissions in the EU, driving the need for sustainable construction practices. Software solutions that can accurately model energy performance, calculate carbon footprints, and ensure compliance with environmental regulations are in high demand. As per the World Green Building Council, the trend towards net-zero carbon buildings is accelerating, with a vision that by 2030, all new buildings will have at least 40 percent less embodied carbon and be net-zero operational carbon. Construction software providers can integrate life cycle assessment tools and sustainability dashboards into their platforms to help architects and contractors meet these targets. The ability to simulate different material choices and design scenarios for their environmental impact allows for more sustainable decision-making. Furthermore, regulatory bodies are increasingly requiring digital documentation of sustainability metrics, which can be efficiently managed through specialized software. The growing consumer preference for eco-friendly buildings also drives developers to seek tools that verify and certify green credentials. By offering comprehensive sustainability modules, software vendors can address a critical pain point for the industry. This alignment with regulatory and market trends positions sustainability-focused software as a key growth area. The integration of these tools supports the broader societal goal of reducing the environmental impact of the built environment.

MARKET CHALLENGES

Fragmentation and lack of interoperability among diverse software platforms

The highly fragmented nature of the construction software landscape, coupled with a lack of seamless interoperability between different platforms, poses a significant challenge to the growth and efficiency of the overall European construction software market. The European construction industry utilizes a wide variety of software solutions from different vendors, each with proprietary data formats and interfaces. According to the European Construction Industry Federation (FIEC), the lack of standardized data exchange protocols hinders the digital transformation of the construction sector and effective collaboration among project stakeholders who often use incompatible tools and data formats. This fragmentation leads to data silos where critical information is trapped within specific applications, making it difficult to achieve a holistic view of the project. As per the buildingSMART International organization, the absence of universal open standards results in significant time and cost wasted on manual data entry and error correction when transferring information between systems. Although initiatives like Industry Foundation Classes aim to address this issue, widespread adoption and consistent implementation remain elusive. Contractors often struggle to integrate project management software with design tools, accounting systems, and supply chain platforms. This disconnect reduces the overall value of digital investments and frustrates users who expect seamless workflows. The complexity of managing multiple software licenses and versions further exacerbates the problem. Without true interoperability, the promise of integrated digital construction remains unfulfilled. Vendors face the challenge of developing flexible APIs and adhering to open standards while protecting their intellectual property. Technical barriers currently constrain the full potential of digital transformation in the European construction sector. This will remain the case until a more unified ecosystem emerges.

Cybersecurity risks and data privacy concerns in cloud- based solutions

The construction industry’s growing dependence on cloud-based software brings significant cybersecurity risks and data privacy concerns, which impede the expansion of the Europe construction software market. These issues continue to hinder the broad adoption of and confidence in digital solutions. Construction projects involve sensitive data, including proprietary designs, financial information, and personal data of workers and clients, which are attractive targets for cybercriminals. According to the European Union Agency for Cybersecurity, the construction sector has become an increasingly frequent target for ransomware attacks and data breaches due to its relatively lower level of cyber maturity compared to other industries. The migration of data to cloud environments expands the attack surface, requiring robust security measures that many construction firms may lack the expertise to implement effectively. As per the General Data Protection Regulation (GDPR), strict requirements govern the handling of personal data, imposing heavy fines, up to €20 million or 4% of total global annual turnover, for non-compliance, which adds a layer of legal complexity for data controllers and processors (including software providers managing user data). Concerns about data sovereignty and the location of servers also persist among European clients who prefer to keep their data within EU borders. The fear of intellectual property theft through insecure platforms discourages some firms from fully embracing cloud-based collaboration tools. Additionally, the interconnected nature of modern construction sites with Internet of Things devices increases vulnerability to cyber-physical attacks. Software vendors must continuously invest in advanced encryption, multi-factor authentication, and regular security audits to mitigate these risks. However, maintaining high security standards increases the cost of software and may complicate the user experience. Balancing ease of use with rigorous security remains a persistent challenge. Any high-profile security incident can severely damage trust and slow down market adoption.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

8.86% |

|

Segments Covered |

By Type, Deployment Mode, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Autodesk, Inc., Trimble Inc., Nemetschek Group, Dassault Systèmes, Oracle Corporation, SAP SE, Bentley Systems, Incorporated, Procore Technologies, Inc., RIB Software SE, Asite Solutions Limited |

SEGMENTAL ANALYSIS

By Type Insights

The project management segment was the largest segment in the Europe construction software market and occupied a share of 35.5% in 2025. This prominence of the segment is supported by the critical need for centralized coordination and real-time visibility across complex construction projects involving multiple stakeholders. The inherent complexity of modern construction endeavors necessitates robust tools to manage schedules, resources, and communications effectively. A main fuel for the dominance of project management software is the urgent requirement for centralized coordination and real-time visibility in an industry plagued by fragmentation and communication gaps. Construction projects typically involve architects, engineers, contractors, subcontractors, and clients who must collaborate seamlessly to avoid costly delays and errors. Project management software provides a unified platform where all stakeholders can access up-to-date information regarding timelines, budgets, and task assignments. By centralizing data, these solutions reduce the risk of miscommunication and ensure that all parties are working with the same accurate information. The ability to track progress in real time allows project managers to identify bottlenecks early and implement corrective measures promptly. This proactive approach minimizes downtime and ensures that projects stay on schedule.

Furthermore, the integration of mobile applications enables field workers to update status reports instantly, enhancing the accuracy of data available to office-based managers. The growing complexity of infrastructure projects in Europe, which often span multiple regions and jurisdictions, further amplifies the need for such comprehensive coordination tools. The shift towards collaborative contracting models also favors the adoption of platforms that facilitate transparency and trust among partners. Consequently, project management software has become indispensable for maintaining operational efficiency and delivering projects successfully in the competitive European market. The seamless integration of project management software with Building Information Modeling and other advanced technologies significantly drives its market domination. Modern construction projects rely heavily on BIM for detailed digital representations of physical and functional characteristics of facilities. Project management software that can ingest and visualize BIM data allows teams to link schedule activities directly to specific building components, enabling 4D simulation and better planning. This connectivity reduces manual data entry errors and ensures that changes in the design model are automatically reflected in the project schedule and resource plans. The integration with Internet of Things sensors further enhances capabilities by providing real-time data on equipment usage, material levels, and environmental conditions. This holistic view enables more accurate forecasting and risk management. Additionally, the combination with artificial intelligence allows for predictive analytics, helping managers anticipate potential delays or cost overruns based on historical data and current trends. The ability to offer a comprehensive ecosystem rather than a standalone tool makes integrated project management software more attractive to large construction firms. This technological synergy creates a sticky user environment where switching costs are high, thereby reinforcing the market position of leading providers. The continuous evolution of these integrations ensures that project management software remains at the core of digital transformation in the European construction sector.

The quality and safety segment is likely to experience the fastest CAGR of 12.5% during the forecast period. This quick surge of the segment is propelled by stringent regulatory requirements and the increasing prioritization of worker welfare and compliance in the European construction industry. The imposition of stringent regulatory requirements and compliance mandates across European countries is a primary catalyst for the rapid growth of quality and safety software. The European Union and individual member states have implemented rigorous health and safety regulations to protect workers and ensure the structural integrity of buildings. Software solutions that automate safety inspections, incident reporting, and compliance tracking help companies meet these legal obligations efficiently. The introduction of the European Pillar of Social Rights further emphasizes the right to safe and healthy working conditions, driving companies to invest in tools that enhance safety monitoring. Non-compliance with these regulations can result in severe penalties, project stoppages, and reputational damage, making digital compliance tools essential. The software enables real-time documentation of safety audits and immediate identification of hazards, reducing the likelihood of accidents.

Furthermore, the digitization of safety records provides auditable trails that simplify regulatory inspections and insurance claims. The increasing focus on corporate social responsibility also prompts firms to demonstrate their commitment to safety through transparent reporting. As regulations continue to evolve and tighten, the demand for agile and comprehensive safety management software will continue to surge. This regulatory pressure ensures that quality and safety solutions remain a high priority for construction firms across Europe. The growing emphasis on worker welfare and proactive risk mitigation is significantly accelerating the adoption of quality and safety software in the European construction market. Construction companies are increasingly recognizing that investing in safety not only fulfills legal duties but also improves morale, reduces absenteeism, and enhances overall productivity. Quality and safety software enables the implementation of proactive risk management strategies by identifying potential hazards before they result in incidents. These platforms often include features for near-miss reporting, allowing teams to learn from close calls and prevent future occurrences. The integration of wearable technology and Internet of Things devices with safety software provides real-time monitoring of worker health and location, enabling immediate response in case of emergencies. This technological capability is particularly valuable in large and complex construction sites where visibility is limited. The focus on mental health and well-being is also gaining traction with software offering resources and tracking mechanisms for worker support. Companies that prioritize safety through advanced software solutions are better positioned to attract and retain skilled labor in a competitive market. The reputation for safety excellence also enhances a company’s ability to win contracts, particularly from public sector clients who prioritize ethical and safe practices. This cultural shift towards prioritizing human capital drives the sustained growth of the quality and safety software segment.

By Deployment Mode Insights

The cloud deployment mode segment held the majority share of 60.1% of the Europe construction software market in 2025. This supremacy of the segment is credited to the flexibility, scalability, and cost-effectiveness of cloud-based solutions, which align well with the dynamic and distributed nature of construction projects. The superior flexibility and accessibility offered by cloud-based deployment are key factors driving its dominance in the Europe construction software market. Construction projects often involve teams working across multiple locations, including offices,s construction sites, and remote supplier facilities. Cloud-based software allows users to access critical data and applications from any device with an internet connection, facilitating seamless collaboration. This trend is particularly pronounced in construction, where real-time access to project updates, drawings, and schedules is essential for decision-making. Cloud platforms eliminate the need for physical presence in the office, enabling field engineers and site managers to update progress and resolve issues instantly. This immediacy reduces delays and improves the responsiveness of the project team.

Furthermore, cloud solutions support simultaneous access by multiple users, ensuring that everyone is working with the most current information. The elimination of version control issues common with file-based systems enhances data integrity and reduces errors. The scalability of cloud infrastructure allows companies to adjust their computing resources based on project demands without significant upfront investment in hardware. This agility is crucial for construction firms that experience fluctuating workloads. The ease of deployment and minimal maintenance requirements further contribute to the preference for cloud-based solutions. As mobile connectivity improves across Europe, the advantages of cloud accessibility become even more pronounced, solidifying its position as the leading deployment mode. The cost-effectiveness and reduced burden on IT infrastructure associated with cloud deployment are major drivers of its leading position in the market. Traditional on-premises software requires significant capital expenditure for servers, storage, and networking equipment, as well as ongoing costs for maintenance, upgrades, and security. Cloud-based software operates on a subscription model, which converts capital expenditure into predictable operational expenditure, making it more affordable for smaller firms. The service provider manages all backend infrastructure, including security patches and software updates, relieving construction companies of these technical responsibilities. This allows firms to focus their internal IT resources on strategic initiatives rather than routine maintenance. The pay-as-you-go model enables companies to scale their software usage up or down based on project needs, avoiding waste from unused licenses. Additionally, cloud providers often offer robust disaster recovery and backup services, which would be prohibitively expensive for individual companies to implement on their own. This enhanced security and reliability at a lower cost is a compelling value proposition. The reduction in energy consumption associated with shared cloud data centers also aligns with sustainability goals. These financial and operational advantages make cloud deployment the preferred choice for a wide range of construction organizations across Europe.

The cloud segment is also the fastest-growing deployment mode in the Europe construction software market with a projected CAGR of 14.2% from 2026 to 2034 due to the accelerating digital transformation in the industry and the increasing acceptance of software as a service models. Also, the accelerating pace of digital transformation in the European construction industry is a key driver for the rapid growth of cloud-based software deployment. As construction firms increasingly recognize the benefits of digitization, they are shifting away from legacy on-premises systems towards modern Software as a Service solutions. The construction sector is catching up with this trend as companies seek to leverage advanced technologies such as artificial intelligence and big data analytics, which are more easily accessible via cloud platforms. The ease of integrating third-party applications and APIs in cloud environments fosters innovation and allows for customized solutions. The rapid deployment capabilities of cloud software enable firms to implement new tools quickly without lengthy installation processes. This agility is crucial in a fast-paced industry where time to value is important. The growing familiarity with cloud services among younger workers entering the workforce also reduces resistance to adopting

on. Furthermore, the availability of high-speed internet connections across Europe, including rural areas where many construction sites are located, supports the reliable use of cloud applications. The shift towards remote work and hybrid models post-pandemic has further normalized the use of cloud-based collaboration tools. This cultural and technological shift ensures that cloud deployment will continue to grow at an accelerated rate, outpacing traditional on-premises solutions

. Contrary to initial perceptions, the enhanced security and data privacy features offered by leading cloud providers are driving the rapid growth of this deployment mode in the Europe construction software market. Major cloud service providers invest heavily in state-of-the-art security infrastructure, including encryption, multi-factor authentication, and continuous monitoring, which often exceeds the capabilities of individual construction firms. The implementation of the General Data Protection Regulation in Europe has raised awareness about data privacy, requiring companies to handle personal and sensitive project data with utmost care. Construction companies are increasingly confident in the ability of cloud providers to protect their data from cyber threats such as ransomware and data breaches. The ability to define granular access controls ensures that only authorized personnel can view or modify sensitive information. Regular automated backups and disaster recovery options provided by cloud services further mitigate the risk of data loss. The transparency of security practices and compliance with international standards build trust among users. As cyber threats become more sophisticated, the collective defense offered by cloud providers becomes more attractive. This reassurance regarding security and privacy removes a significant barrier to adoption, allowing more firms to embrace cloud deployment. The continuous improvement of security features by providers ensures that cloud platforms remain secure and reliable, fostering sustained growth.

By Application Insights

The general contractors segment dominated the Europe construction software market and accounted for a 40.6% share in 2025. This dominance of the segment is driven by the central role general contractors play in managing complex projects and their need for comprehensive tools to coordinate various aspects of construction. General contractors hold the dominant position in the market due to their central role in coordinating and managing all aspects of construction projects from inception to completion. They are responsible for overseeing subcontractors, managing schedules, controlling budgets, and ensuring quality and safety standards are met. This pivotal position requires them to handle vast amounts of data and communicate with diverse stakeholders, making robust software solutions essential. Software tools enable them to integrate information from design procurement, and field operations into a single coherent view. The ability to monitor progress in real time allows general contractors to make informed decisions and address issues proactively. The complexity of modern construction projects, which often involve multiple phases and disciplines, further increases the reliance on digital management tools. General contractors are also under pressure to demonstrate transparency and accountability to clients, which is facilitated by detailed reporting features in construction software. The need to optimize resource allocation and minimize waste drives the adoption of advanced planning and scheduling modules. Furthermore, general contractors often mandate the use of specific software platforms for subcontractors to ensure seamless data exchange and collaboration. This influence extends the reach of their software choices throughout the supply chain. The strategic importance of efficient management in maintaining competitive bids and successful project delivery cements the leading position of general contractors in the software market. Their extensive requirements drive innovation and feature development in construction software solutions. The intense pressure to improve profit margins and operational efficiency is a significant driver for the widespread adoption of construction software among general contractors in Europe. The construction industry is characterized by low profit margins and high volatility, making cost control a critical success factor. General contractors are increasingly turning to software solutions to identify inefficiencies and optimize processes. Software enables precise monitoring of labor and material costs, allowing contractors to detect deviations from the budget early. The automation of administrative tasks such as invoicing and procurement reduces overhead costs and frees up resources for core activities. The ability to analyze historical data helps in creating more accurate bids, reducing the risk of underpricing projects.

Furthermore,e improved efficiency through better scheduling and resource management leads to faster project completion, which enhances cash flow. The competitive landscape in Europe forces general contractors to differentiate themselves through operational excellence, which is supported by advanced software capabilities. The integration of financial management tools with project management platforms provides a holistic view of project performance. This comprehensive approach enables data-driven decision-making that enhances profitability. The continuous drive to do more with less in a challenging economic environment ensures that general contractors remain the primary adopters of construction software. Their focus on bottom-line results drives the demand for solutions that deliver tangible economic benefits.

The architects and engineers segment is expected to exhibit a noteworthy CAGR of 11.8% over the forecast period, owing to the increasing complexity of building designs and the mandatory adoption of Building Information Modeling in the design phase. In addition, the mandatory adoption of Building Information Modeling in the design phase is a primary driver for the rapid growth of software usage among architects and engineers in Europe. Governments across the region are increasingly requiring BIM for public infrastructure projects to improve design quality and reduce errors. Architects and engineers are the primary creators of BIM models, making them the first adopters of related software technologies. This early integration of digital tools reduces the likelihood of costly changes during later stages of the project. The complexity of modern architectural designs, which often involve sustainable features and smart building technologies, requires advanced software for accurate modeling and simulation. Engineers use specialized software for structural analysis, energy modeling, and system design, which are integral parts of the BIM workflow. The need for interdisciplinary collaboration between architects and engineers further drives the adoption of compatible software platforms. The ability to share and coordinate models in real time enhances design efficiency and accuracy. Furthermore, the requirement for digital deliverables at the handover stage necessitates the use of sophisticated design tools from the outset. The continuous evolution of BIM standards and regulations ensures that architects and engineers must keep their software skills and tools up to date. This regulatory and technical push creates a sustained demand for advanced design and engineering software. The focus on precision and compliance in the design phase establishes this segment as a key growth area in the market. The increasing integration of sustainable design and performance analysis tools in architectural and engineering software is accelerating growth in this segment. The European Green Deal and related regulations mandate strict energy efficiency and sustainability standards for new buildings driving the need for specialized design capabilities. Software solutions that enable life cycle assessment, energy simulation, and daylight analysis are becoming essential tools in the design process. These tools allow designers to evaluate different material choices and design scenarios for their environmental impact, enabling informed decision-making. The ability to simulate building performance under various conditions helps in optimizing passive design strategies and renewable energy integration. The growing demand for green building certifications such as BREEAM and LEED further necessitates the use of software that can track and verify sustainability metrics. Architects and engineers are increasingly incorporating these tools into their workflows to meet client expectations and regulatory requirements. The integration of artificial intelligence in design software also aids in generating optimized, sustainable designs automatically. This technological advancement reduces the time and effort required for complex simulations. The focus on sustainability is not just a regulatory requirement but also a market differentiator for design firms. The continuous innovation in green design software ensures that this segment remains at the forefront of market growth. The alignment with broader societal goals for environmental protection sustains the demand for these specialized tools.

REGIONAL ANALYSIS

Germany Construction Software Market Analysis

Germany led the Europe construction software market and occupied a 20.4% share in 2025. A resilient construction industry, combined with extensive manufacturing capabilities and a pioneering approach to digital technology in design and engineering, drives the country’s dominance. The German construction sector is characterized by a high degree of professionalism and a strong emphasis on quality and precision, which drives the demand for advanced software solutions. According to the Federal Statistical Office (Destatis), the building sector represents a major pillar of the national economy, contributing a substantial portion of total industrial revenue through both residential and commercial development projects. This large volume of activity creates a substantial market for software tools that enhance efficiency and manage complexity. The presence of leading engineering and architectural firms in Germany fosters a culture of innovation and digital adoption. As per the German Association for Building Information Modeling, the country has established clear standards and guidelines for BIM implementation, which accelerates the uptake of related software. The strong industrial base provides a steady demand for commercial and industrial construction projects, which often require sophisticated management and design tools. The government’s initiative to promote digitalization in the construction sector through the Planen Bauen 4.0 platform further supports market growth. This initiative aims to establish BIM as the standard method for planning and executing construction projects. The high level of technical expertise among German professionals facilitates the effective use of complex software applications. The focus on sustainability and energy efficiency in German building regulations also drives the adoption of performance analysis tools. The strong export orientation of German construction and engineering firms encourages the use of internationally compatible software standards. The continuous investment in research and development by German software vendors ensures a steady supply of innovative solutions. The robust infrastructure and high internet penetration support the widespread use of cloud-based applications. These factors collectively sustain Germany’s position as the largest market for construction software in Europe.

United Kingdom Construction Software Market Analysis

The United Kingdom was the second largest country in the Europe construction software market and secured a 18.2% share in 2025. Its pioneering role in Building Information Modeling mandates and a mature construction industry that values digital efficiency fuel the growth of the UK market. The UK was one of the first countries in Europe to mandate the use of BIM for publicly funded projects, which has created a deeply ingrained culture of digital construction. According to the UK Government, the transition toward standardized digital information management has been a central policy requirement for years, compelling the construction supply chain to utilize modern data-sharing platforms and software. This early start has given the UK a significant advantage in terms of software maturity and user proficiency. As per the National Building Specification, the majority of large construction firms in the UK now use BIM as a standard practice, creating sustained demand for advanced software tools. The presence of major global construction and engineering companies headquartered in the UK further boosts the market. The UK construction industry faces significant challenges related to productivity and skills shortage, which drives the adoption of software solutions that automate tasks and improve efficiency. According to the Construction Leadership Council, digital transformation is seen as a key strategy for addressing these challenges. The strong focus on infrastructure development, including transport and energy projects, requires sophisticated project management and design software. The regulatory environment in the UK emphasizes safety and quality, which is supported by digital compliance tools. The vibrant tech sector in London and other cities fosters innovation in construction technology with numerous startups developing niche software solutions. The availability of skilled IT professionals supports the implementation and maintenance of complex software systems. The post Brexit focus on domestic infrastructure investment continues to drive construction activity and software demand. The established ecosystem of software vendors, consultants, and training providers ensures a supportive environment for market growth. These factors maintain the UK’s strong position in the European market.

France Construction Software Market Analysis

France plays a major role in the Europe construction software market due to its large public infrastructure programs and increasing regulatory push for digitalization in the construction sector. The French construction industry is undergoing a significant digital transformation driven by government initiatives and the need to improve productivity. The Plan BIM (formerly Plan BIM 2022) serves as the national strategy to generalize digital tool usage and improve professional skills across the construction sector. This strategic plan provides funding and support for training and software adoption, particularly for small and medium-sized enterprises. As per the French Building Federation, the use of BIM is becoming increasingly common in large-scale projects driven by client demand and regulatory expectations. The extensive public infrastructure projects in France, including high-speed rail lines and urban renewal programs, require advanced project management and design software. The presence of major international construction companies in France, such as Vinci and Bouygues, drives the adoption of enterprise-level software solutions. These companies are leaders in digital construction and set standards for the wider industry. The regulatory framework in France is evolving to include stricter requirements for energy performance and sustainability, which drives the demand for analysis and simulation tools. The growing awareness of the benefits of digital collaboration among French architects and engineers further supports market growth. The education system in France is increasingly incorporating digital construction skills into curricula, ensuring a future workforce proficient in software use. The vibrant startup ecosystem in Paris contributes to the development of innovative construction technology solutions. The focus on renovating existing building stock to improve energy efficiency creates opportunities for software tools that support retrofitting projects. These dynamics ensure that France remains a key market for construction software in Europe.

Italy Construction Software Market Analysis

Italy witnessed a consistent growth in the Europe construction software market owing to significant government incentives for building renovation and a gradual but steady adoption of digital construction practices. The Italian construction market has experienced a surge in activity due to the Superbonus 110 percent scheme, which provided tax incentives for energy efficiency renovations. The National Agency for New Technologies, Energy and Sustainable Economic Development (ENEA) shows that renovation incentives have spurred massive construction volume, requiring digital tools for complex compliance. While the scheme has changed, the legacy of increased digital awareness remains. As per the Italian Building Confederation, there is a growing recognition of the need for digitalization to manage the complexity of renovation projects and ensure compliance with strict energy standards. The adoption of BIM is gradually increasing in Italy, driven by public procurement laws that encourage its use for large projects. The presence of a strong design and architectural heritage in Italy fosters a demand for high-quality design software. Italian architects and engineers are known for their creativity, which is supported by advanced modeling and visualization tools. The fragmentation of the Italian construction industry, with many small firms, presents a challenge but also an opportunity for cloud-based software providers offering affordable and easy-to-use solutions. The government’s National Recovery and Resilience Plan includes investments in digital infrastructure and skills, which support the long-term growth of the construction software market. The increasing focus on seismic safety and structural integrity also drives the demand for specialized engineering software. The gradual modernization of the industry and the entry of younger digitally native professionals are shifting cultural attitudes towards technology. These factors contribute to the steady growth of the construction software market in Italy.

Netherlands Construction Software Market Analysis

The Netherlands is anticipated to expand significantly in the Europe construction software market during the forecast period due to its progressive approach to digital construction and strong emphasis on sustainability and innovation. It is a leader in digital construction in Europe with a highly collaborative industry culture that embraces innovation. The Central Government Real Estate Agency requires specific digital modeling standards for public works, part of a long-term effort to integrate information management in the built environment. Thilong-standing support has created a mature market where digital workflows are the norm. According to Bouwend Nederland, most major construction companies have adopted digital platforms for project coordination, though the industry continues to work toward full optimization of these tools. The country’s focus on sustainability and circular economy principles drives the demand for software tools that support life cycle assessment and material tracking. The dense urban environment and complex infrastructure projects in the Netherlands require precise planning and coordination, which is facilitated by advanced software solutions. The presence of leading global software companies and tech hubs in the Netherlands fosters a vibrant ecosystem for construction technology innovation. The high level of English proficiency and international orientation of the Dutch construction industry facilitates the adoption of global software standards. The strong emphasis on water management and hydraulic engineering also creates a niche demand for specialized simulation and design software. The collaborative contracting models popular in the Netherlands, such as Integrated Project Delivery, rely heavily on shared digital platforms. The continuous investment in digital skills and education ensures a workforce capable of leveraging advanced tools. These factors position the Netherlands as a key innovator and adopter in the European construction software market.

COMPETITION OVERVIEW

The competition in the Europe construction software market is characterized by a dynamic mix of established global giants and innovative regional specialists who vie for dominance through technological advancement and service excellence. Large multinational corporations leverage their extensive resources to offer integrated suites that cover the entire construction lifecycle from design to facility management. These players compete on the breadth of their offerings and their ability to provide seamless interoperability between different modules. Meanwhile, niche providers focus on specialized solutions for specific tasks such as cost estimation or safety management, allowing them to capture dedicated segments of the market. The market is witnessing intense rivalry as companies strive to differentiate themselves through the integration of emerging technologies like artificial intelligence and the Internet of Things. Customer retention is a key battleground, with vendors focusing on user experience and customer support to reduce churn rates. The shift toward cloud-based subscription models has lowered barriers to entry for new competitors, increasing the pace of innovation. Strategic partnerships and ecosystems are becoming crucial as no single vendor can meet all customer needs independently. Price competition is moderate, but value-driven differentiation is more prevalent as clients seek solutions that deliver measurable productivity gains. Regulatory compliance and data security are also significant competitive factors, particularly in Europe, where strict standards apply. The market remains fragmented, but consolidation trends are evident as larger firms acquire smaller innovators to enhance their capabilities. This competitive landscape drives continuous improvement and benefits end users through better tools and services.

KEY MARKET PLAYERS

A few major players of the Europe construction software market include

- Autodesk, Inc

- Trimble Inc

- Nemetschek Group

- Dassault Systèmes

- Oracle Corporation

- SAP SE

- Bentley Systems

- Incorporated

- Procore Technologies, Inc

- RIB Software SE

- Asite Solutions Limited

Top Strategies Used by the Key Market Participants

Key players in the Europe construction software market primarily focus on strategic acquisitions to expand their product portfolios and integrate complementary technologies. Companies actively pursue mergers with niche software providers to offer comprehensive end-to-end solutions that cover all phases of the construction lifecycle. Another major strategy is the development of open platforms and application programming interfaces that facilitate interoperability and data exchange between different systems. This approach addresses the industry need for seamless collaboration and reduces fragmentation. Providers are also investing heavily in cloud computing infrastructure to enable real-time access and scalability for users across diverse locations. The integration of artificial intelligence and machine learning is a critical strategy to enhance predictive analytics and automate routine tasks, thereby improving efficiency. Sustainability is increasingly becoming a central theme, with vendors developing tools that help users measure and reduce the environmental impact of construction projects. Partnerships with technology firms and educational institutions are common to foster innovation and develop digital skills within the workforce. Companies also emphasize user experience improvements to ensure their software is intuitive and accessible to professionals with varying technical backgrounds. These strategies collectively aim to drive digital transformation and deliver tangible value to customers in a competitive market environment.

Leading Players in the Europe Construction Software Market

- Autodesk stands as a global leader in design and engineering software with a profound impact on the European construction sector. The company provides essential tools such as Revit and AutoCAD, which are industry standards for Building Information Modeling and computer-aided design. Autodesk contributes significantly to the global market by driving digital transformation through its comprehensive cloud-based platforms that facilitate collaboration among architects, engineers, and contractors. Recent actions to strengthen its position include the continuous enhancement of its Autodesk Construction Cloud, which integrates design and build phases seamlessly. The company has also invested heavily in artificial intelligence capabilities to automate routine tasks and provide predictive insights for project management. By fostering an open ecosystem through application programming interfaces, Autodesk enables third-party developers to create specialized solutions that extend the functionality of its core products. This strategy ensures that their software remains adaptable to the diverse needs of the European construction industry. Autodesk actively engages in partnerships with local governments and educational institutions to promote digital skills and standardize BIM adoption across the region. Their commitment to sustainability is evident in tools that help users analyze and reduce the carbon footprint of building projects. These initiatives solidify Autodesk’s role as a pivotal enabler of innovation and efficiency in the global construction landscape.

- Nemetschek is a prominent provider of software solutions for the architecture, engineering, and construction industries with a strong heritage in Europe. The company offers a diverse portfolio, including brands such as Allplan, Graphisoft, and Bluebeam, which cater to various stages of the construction lifecycle. Nemetschek contributes to the global market by providing specialized tools that address specific regional regulatory requirements and workflow preferences. Their recent strategy focuses on expanding their Open BIM approach, which promotes interoperability and data exchange between different software platforms. The company has strengthened its market position through strategic acquisitions of niche software providers that enhance its capabilities in areas such as structural analysis and facility management. Nemetschek is also investing in cloud technologies to enable real-time collaboration and data accessibility for distributed teams. Their emphasis on user experience and intuitive design ensures that their tools are accessible to professionals with varying levels of technical expertise. The company actively supports industry initiatives aimed at standardizing digital processes and improving productivity in the construction sector. By focusing on sustainable building practices, Nemetschek develops solutions that help users optimize energy efficiency and material usage. Their global presence, combined with deep local knowledge, allows them to serve a wide range of clients effectively. This balanced approach ensures continued relevance and growth in the competitive European software market.

- Oracle plays a significant role in the Europe construction software market through its robust enterprise resource planning and project management solutions. The company’s Primavera and Aconex platforms are widely used by large construction firms for managing complex projects and ensuring operational efficiency. Oracle contributes to the global market by providing scalable cloud-based infrastructure that supports the extensive data requirements of major infrastructure projects. Recent actions to strengthen its position include the integration of advanced analytics and machine learning capabilities into its construction management suite. These technologies enable users to predict risks, optimize schedules, and control costs more effectively. Oracle has also focused on enhancing the connectivity between its financial management and project execution tools to provide a holistic view of project performance. The company actively collaborates with industry partners to develop standardized data models that facilitate seamless information exchange. Their commitment to security and compliance ensures that sensitive project data is protected in accordance with stringent European regulations. Oracle continues to invest in training and support services to help customers maximize the value of their software investments. By leveraging its extensive experience in enterprise software, Oracle provides reliable and comprehensive solutions that meet the demanding needs of the construction industry. This focus on integration and intelligence helps clients achieve greater transparency and control over their operations.

MARKET SEGMENTATION

This research report on the European construction software market has been segmented and sub-segmented based on type, deployment mode, application & region.

By Type

- Project Management

- Financial Management

- Quality And Safety

- Field Productivity

- Others

By Deployment Mode

By Application

- General Contractors

- Building Owners

- Architects And Engineers

- Specialty Contractors

- Sub-Contractors

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe