7 Ways to Turn It Around

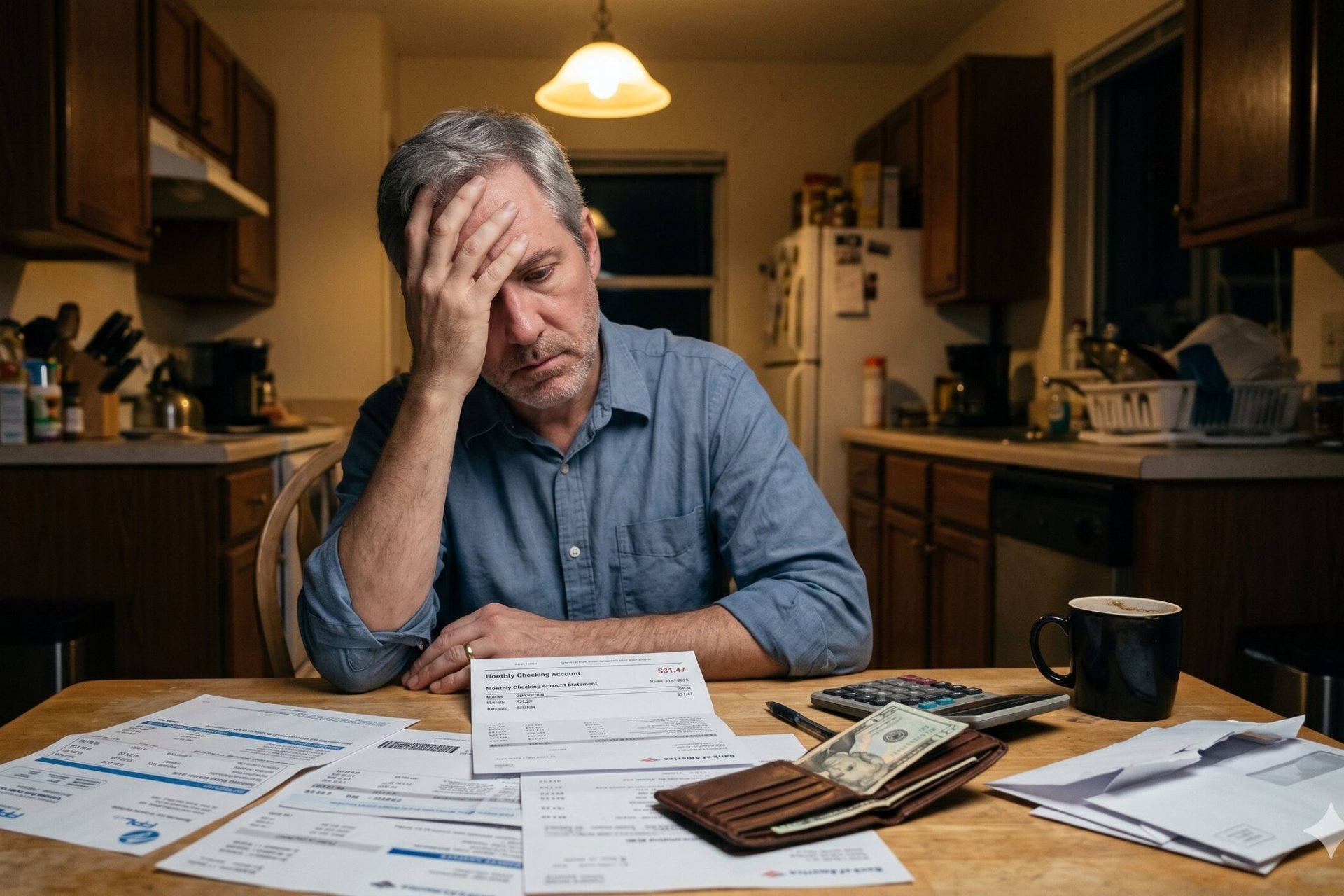

Your transmission gives out on a Tuesday. The bill is $2,800. Your checking account has $312.

Welcome to America’s quietest financial crisis.

Nearly 1 in 4 American households spent more than 95% of their income on necessities last year, according to a Bank of America Institute analysis — leaving almost no margin for the unexpected. Self-reported surveys put the number even higher.

If you’ve ever lived there, you know how stressful it is. What most people don’t see is how much “no buffer” keeps costing even after they escape — quietly draining money for years.

I’ve watched this pattern for more than 40 years, and the math always works the same. People without savings don’t just pay more when emergencies hit. They pay more for everything. They make worse decisions. They miss opportunities other people grab.

Here are seven ways living one paycheck from disaster keeps stealing money you should be keeping.

1. A $400 surprise becomes years of credit card debt

The Federal Reserve’s most recent household economic survey found 37% of American adults couldn’t cover a $400 emergency expense with cash. Another 18% said the largest emergency they could handle from savings was under $100.

When the flat tire, vet bill, or busted water heater hits, out comes the credit card. The average APR on cards carrying a balance is now over 21%, per Federal Reserve data.

A $400 charge isn’t a $400 problem at that rate. Paid down slowly, it can balloon into years of compounding interest. Americans collectively owe $1.28 trillion on credit cards right now — most of it the ghost of small emergencies past.

If you’re stuck in that spiral, our guide to the most ruthless ways to destroy credit card debt walks you through every realistic exit.

2. You can’t walk away from a bad job

Every paycheck without a buffer is a hostage situation. The toxic boss, the dead-end role, the company quietly heading for layoffs — you can’t leave because you can’t afford to.

A three- to six-month emergency fund isn’t just protection against car repairs. It’s permission to walk. People with savings negotiate harder, take risks on better opportunities, and don’t tolerate bad situations for fear of missing rent.

The gap in your savings is also a gap in your career, your salary, and your sanity.

3. Small problems become big problems

The cracked windshield you can’t fix becomes an inspection failure. The dental cleaning you skip becomes a root canal. The roof drip you ignore becomes structural rot.

Deferred maintenance is one of the most expensive habits in American life, and it’s almost always driven by thin savings. People who can pay $200 today don’t end up paying $2,000 next year.

Quick aside — most internet financial advice comes from people who weren’t alive during the last recession. I’ve been writing about money for more than 40 years. Want rock-solid advice? Sign up for the free Money Talks Newsletter. Takes 10 seconds. No fluff. No spam.

4. You’re effectively uninsured even when you’re insured

Got a $5,000 health insurance deductible? A $1,000 collision deductible? A $2,500 wind-and-hail deductible on the homeowners policy?

Without cash to cover them, those deductibles might as well be infinite. You’ll either skip the claim, take on debt to use the policy, or — worse — keep driving the wrecked car and leaving the leaking pipe alone.

You’re paying for protection you can’t actually afford to use.

5. You sell at the worst possible time

Some of the best buying opportunities of the last 20 years happened during panics — March 2009 and March 2020 chief among them. The investors who got rich during those crashes had one thing in common: cash to deploy.

Without a buffer, you’re not buying during a crash. You’re selling. Often at the worst possible moment, just to cover the rent.

6. You overpay for almost everything

When you can’t buy ahead, you can’t capitalize on sales, bulk pricing, or annual-payment discounts. You pay full retail because you need it now. You rack up activation fees, late fees, and overdraft fees because timing is everything when you have no slack.

Pay car insurance monthly instead of annually? That’s typically a 5% to 15% surcharge. Same with renters insurance and most subscription services. Every “convenient” monthly payment is a tax on having no savings.

Our roundup of clever ways to slash your monthly bills by $500 shows where to start cutting.

7. You raid retirement and pay twice

When the credit card is maxed and the emergency keeps escalating, the 401(k) becomes the last resort. Early withdrawals before age 59½ trigger a 10% IRS penalty plus full income tax — up to a 30% to 40% haircut. There are a handful of exceptions to that penalty, but they’re narrow and most people don’t qualify.

The bigger cost is the compounding you’ll never get back. Ten thousand dollars pulled at age 40 could’ve grown to more than $50,000 by age 65 in a typical index fund. That’s the real price tag on the emergency you didn’t plan for.

How to start, even if you’re broke right now

Most “build an emergency fund” advice is overwhelming because it sets the bar at six months of expenses. Aim small first.

A starter goal of $1,000 buys you out of the worst credit card spirals. From there, build to one month of essential expenses. Then three. Then six. The first $1,000 is the hardest — and the most important.

Skip a couple of restaurant meals a week and that’s $200 a month. You’ll have $1,000 in five months without changing anything important about your life. If it’s not obvious where you can cut back, take the next step: track your expenses and look hard at where your money is going. Is there anything at all you can cut?

The best expenses to focus on are those you can reduce without negatively impacting your quality of life.

When you do get some money set aside, park it in a high-yield savings account at a separate bank from your checking. Out of sight, out of mind, and earning around 4% while you sleep.

Our guide on building an emergency fund in a high-interest era walks you through where to put it for the best return right now.

Bottom line

Living without a buffer isn’t just a stress problem. It’s a wealth problem, a career problem, and eventually a retirement problem.

The math is simple: Every dollar you keep in reserve is a dollar that doesn’t have to come out of your future at 21% interest. Build it small. Build it slow. But build it, one day at a time. Your future self will thank you.